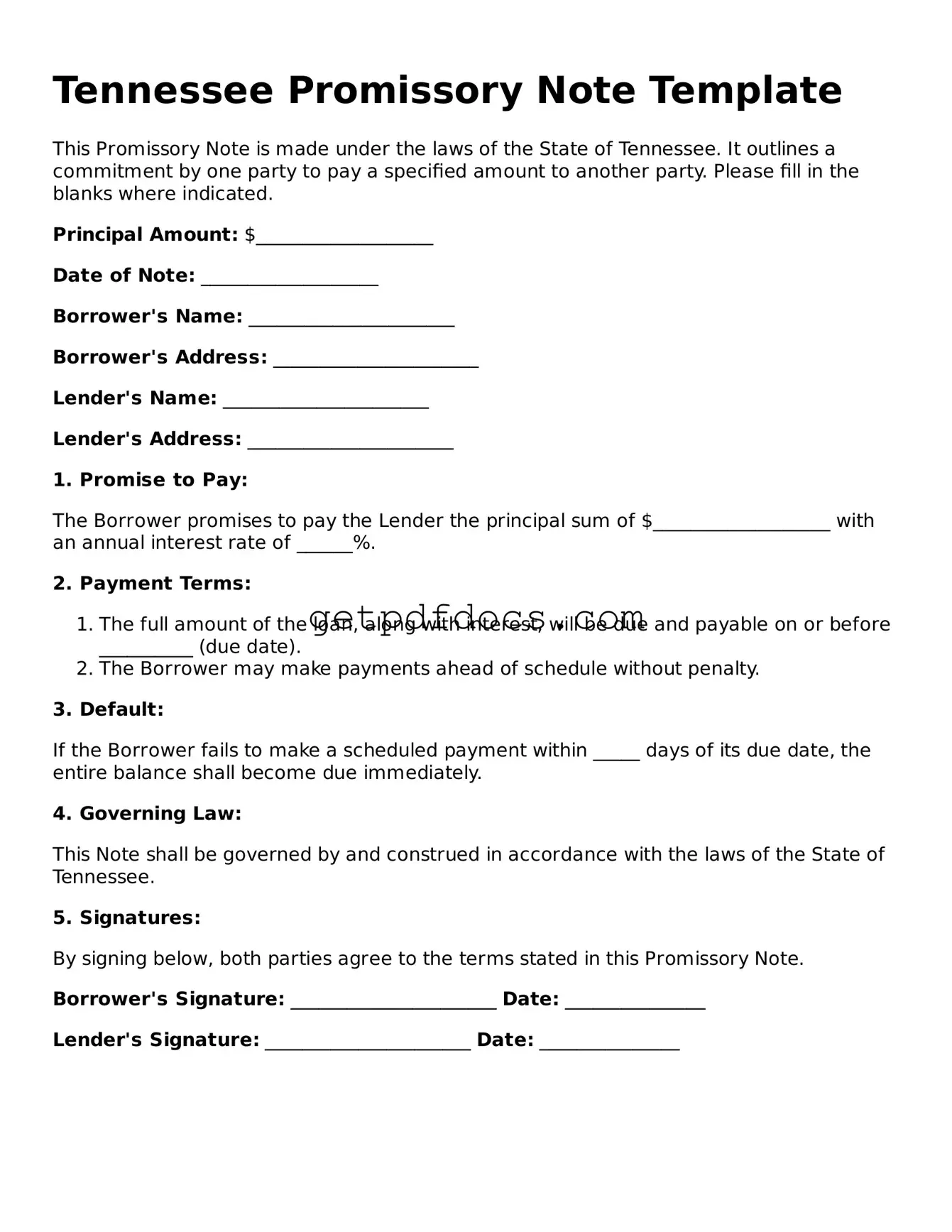

Attorney-Approved Promissory Note Form for Tennessee State

The Tennessee Promissory Note form serves as a vital legal document that outlines the terms of a loan agreement between a lender and a borrower. This form establishes the borrower's promise to repay a specified amount of money, typically with interest, within a defined timeframe. Key components of the form include the principal amount, the interest rate, the payment schedule, and any applicable late fees. Additionally, it may specify collateral if the loan is secured, providing the lender with a means of recourse in case of default. The document requires signatures from both parties, affirming their agreement to the terms laid out within. Understanding the nuances of this form is essential for both lenders and borrowers, as it not only protects their rights but also clarifies their obligations. Proper completion of the Tennessee Promissory Note form can help prevent misunderstandings and disputes, ensuring a smoother lending process.

How to Use Tennessee Promissory Note

After obtaining the Tennessee Promissory Note form, you will need to complete it with specific information regarding the loan agreement. This process involves providing details about the borrower, the lender, the loan amount, and the terms of repayment. Ensure that all information is accurate and clear to avoid any potential disputes in the future.

- Begin by entering the date at the top of the form.

- In the section for the borrower, write the full name and address of the person or entity borrowing the money.

- Next, provide the lender's full name and address in the designated area.

- Clearly state the principal amount of the loan. This is the total amount being borrowed.

- Specify the interest rate, if applicable. Indicate whether it is fixed or variable.

- Outline the repayment schedule. Include the frequency of payments (e.g., monthly, quarterly) and the due date for each payment.

- Indicate any late fees or penalties for missed payments, if relevant.

- Include any additional terms or conditions that both parties have agreed upon.

- Both the borrower and the lender should sign and date the form at the bottom.

Once completed, keep copies for both parties. This document serves as a formal record of the loan agreement and its terms.

Key takeaways

When dealing with a Tennessee Promissory Note, it’s important to understand the essential elements that ensure the document is valid and enforceable. Here are key takeaways to consider:

- Clear Identification of Parties: The note must clearly identify the borrower and the lender. Full names and addresses should be included to avoid any confusion about who is involved in the agreement.

- Loan Amount and Terms: Specify the exact amount being borrowed. Additionally, outline the repayment terms, including interest rates and payment schedules, to ensure both parties understand their obligations.

- Signature Requirement: The borrower must sign the note for it to be legally binding. A signature signifies agreement to the terms laid out in the document.

- Consideration of Legal Terms: While the note should be straightforward, it’s wise to include any legal terms that may protect both parties, such as default conditions or remedies.

- Documentation of Payments: Keep a record of all payments made under the note. This documentation can serve as proof of payment and help avoid disputes in the future.

Understanding these key aspects can simplify the process of creating and utilizing a Tennessee Promissory Note, ensuring that both parties are protected and informed throughout the transaction.

Common mistakes

Filling out a Tennessee Promissory Note form can seem straightforward, but there are common mistakes that many people make. One of the most frequent errors is not including all necessary details. A promissory note should clearly state the amount of the loan, the interest rate, and the repayment schedule. Omitting any of this information can lead to confusion later on.

Another common mistake is failing to sign the document. A promissory note is not legally binding unless it is signed by the borrower. Some individuals may forget to sign or may assume that a verbal agreement is sufficient. Always ensure that both parties sign the note to validate the agreement.

People often overlook the importance of specifying the payment method. Whether payments are to be made by check, bank transfer, or another method, it should be clearly stated in the note. Without this information, misunderstandings can arise, leading to potential disputes over how payments should be made.

Additionally, individuals may neglect to include a date on the note. This is crucial because it establishes when the loan was made and can affect the repayment timeline. Including a clear date helps both parties understand their obligations and protects against any claims of ambiguity in the agreement.

Another mistake involves not addressing what happens in case of default. It’s important to outline the consequences if the borrower fails to make payments as agreed. This could include late fees, legal action, or other remedies. Failing to address this can leave both parties uncertain about their rights and responsibilities.

Lastly, many people do not keep copies of the signed document. Once the promissory note is completed and signed, it’s essential for both parties to retain a copy for their records. This can serve as a reference in the future and can help resolve any disputes that may arise. Always make sure to keep a copy in a safe place.

Documents used along the form

When dealing with a Tennessee Promissory Note, several other forms and documents may be necessary to ensure clarity and legality in the transaction. Each of these documents serves a specific purpose, helping both parties understand their rights and obligations. Below is a list of common forms that are often used alongside a Promissory Note.

- Loan Agreement: This document outlines the terms of the loan, including the amount, interest rate, repayment schedule, and any collateral involved. It provides a comprehensive framework for the loan transaction.

- Security Agreement: If the loan is secured by collateral, this agreement details the assets being used as security. It protects the lender's interest in the event of default.

- Disclosure Statement: This statement provides borrowers with important information about the loan, including costs, terms, and any fees associated with the transaction. It ensures transparency in lending.

- Personal Guarantee: In some cases, a lender may require a personal guarantee from a third party. This document holds the guarantor responsible for the debt if the borrower defaults.

- Payment Schedule: This document outlines the specific dates and amounts of payments due under the Promissory Note. It helps both parties keep track of the repayment process.

- Amendment Agreement: If any terms of the original Promissory Note need to be changed, this document formalizes those changes. It ensures that both parties agree to the new terms.

- RV Bill of Sale: When purchasing a recreational vehicle in Arizona, it’s crucial to fill out the Arizona PDFs to ensure both parties' rights and responsibilities are documented and legally binding.

- Default Notice: If the borrower fails to make payments, this notice informs them of the default. It serves as a formal warning and may outline the consequences of non-payment.

- Release of Liability: Once the loan is fully repaid, this document releases the borrower from any further obligations under the Promissory Note. It provides peace of mind for the borrower.

Understanding these documents can help both borrowers and lenders navigate the lending process more effectively. Each form plays a crucial role in protecting the interests of both parties and ensuring a clear understanding of the loan terms.

Browse Other Common Promissory Note Forms for Different States

Online Promissory Note - A promissory note can be secured or unsecured, depending on the agreement.

Free Promissory Note Template Florida - Promissory notes typically have a simple structure, making them accessible for most borrowers.

Filing the necessary documentation is crucial for any business operating in Florida, and understanding the Florida Sales Tax form is essential. To ensure accuracy in reporting sales and collecting tax, you can find the required form and related resources at floridaforms.net/blank-florida-sales-tax-form/, which provides the guidelines needed for proper submission to the Florida Department of Revenue.

California Promissory Note - The promissory note functions as a key piece in securing financing arrangements.

Frequently Asked Questions

What is a Tennessee Promissory Note?

A Tennessee Promissory Note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender. This note includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. It serves as a binding agreement between the parties involved, ensuring that both understand their rights and obligations.

Who can use a Promissory Note in Tennessee?

Any individual or business in Tennessee can use a Promissory Note. Common users include:

- Individuals borrowing money from friends or family.

- Businesses seeking loans from banks or private lenders.

- Investors lending money for various purposes.

It is essential that both the borrower and lender agree on the terms outlined in the note to avoid future disputes.

What information is typically included in a Tennessee Promissory Note?

A standard Tennessee Promissory Note includes the following information:

- The names and addresses of the borrower and lender.

- The principal amount being borrowed.

- The interest rate, if applicable.

- The repayment schedule, including due dates.

- Any late fees or penalties for missed payments.

- Signatures of both parties, along with the date of signing.

Including all relevant details helps ensure clarity and enforceability of the agreement.

Is a Promissory Note legally binding in Tennessee?

Yes, a Promissory Note is legally binding in Tennessee, provided it meets certain requirements. For the note to be enforceable, it must be signed by the borrower and include clear terms regarding repayment. If the borrower fails to repay as agreed, the lender can take legal action to recover the owed amount.

Can a Promissory Note be modified after it has been signed?

Yes, a Promissory Note can be modified after it has been signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the revised agreement. This ensures that the updated terms are clear and enforceable.

What should I do if a borrower defaults on a Promissory Note?

If a borrower defaults on a Promissory Note, the lender has several options:

- Contact the borrower to discuss the missed payment and seek a resolution.

- Consider offering a revised payment plan if the borrower is experiencing financial difficulties.

- If necessary, pursue legal action to recover the owed amount, which may involve filing a lawsuit.

It is often beneficial to consult with a legal professional before taking any action to ensure the best course is chosen.