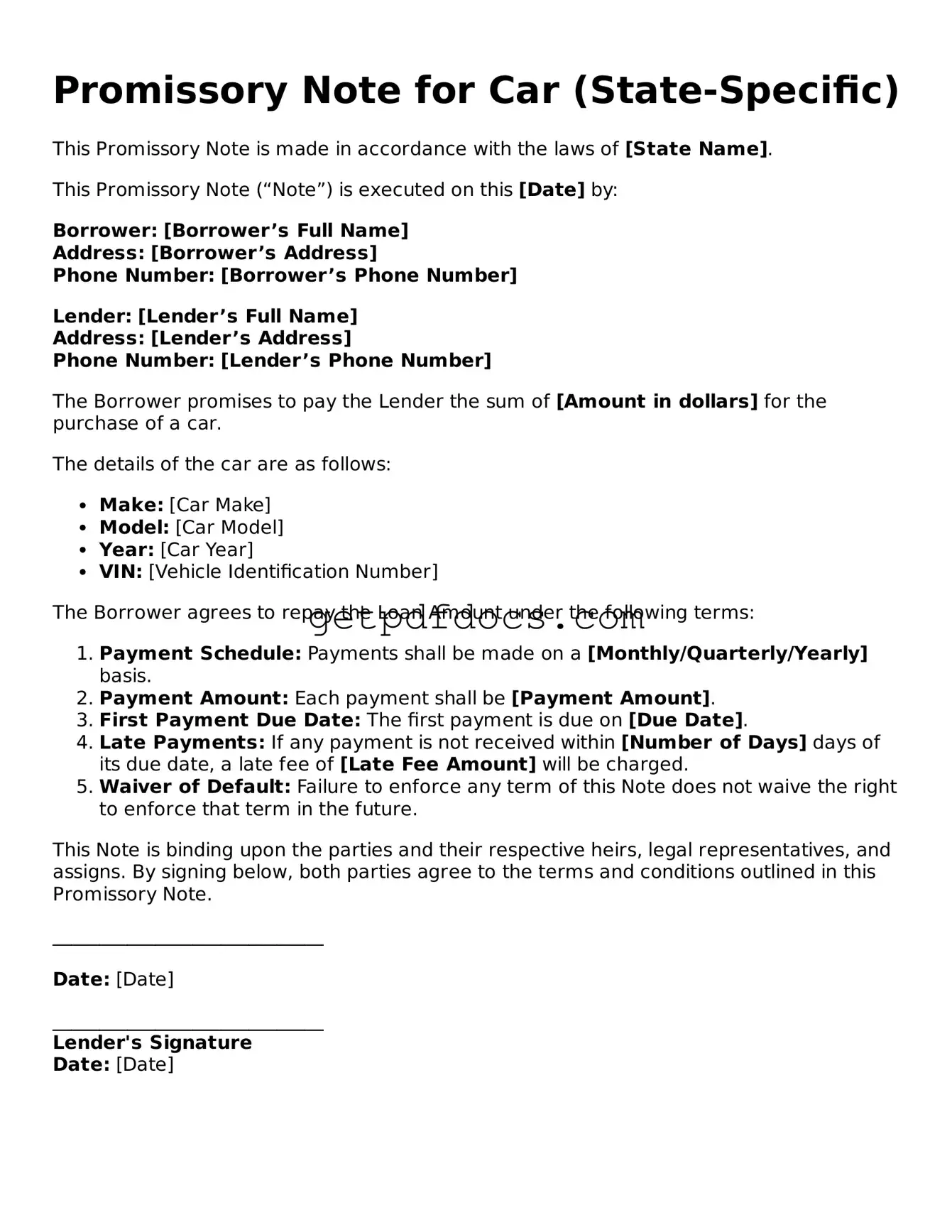

Printable Promissory Note for a Car Template

When purchasing a vehicle, understanding the financial commitments involved is crucial. A Promissory Note for a Car serves as a formal agreement between the buyer and the seller, outlining the terms of the loan used to finance the vehicle. This document not only specifies the amount borrowed but also includes critical details such as the interest rate, repayment schedule, and any penalties for late payments. It is designed to protect both parties by ensuring clarity and accountability throughout the transaction. Additionally, the form may include provisions for securing the loan, which means that the car itself could serve as collateral. This aspect is particularly important, as it provides the lender with a level of security should the borrower default on the loan. Overall, the Promissory Note for a Car is an essential tool that helps facilitate a smooth and transparent exchange, fostering trust between the buyer and the seller while establishing a clear roadmap for repayment.

How to Use Promissory Note for a Car

Once you have the Promissory Note for a Car form in front of you, the next step involves carefully entering the necessary information. This document will outline the terms of your agreement regarding the loan for the vehicle. Accuracy is key to ensure that both parties understand their obligations and rights.

- Title the Document: At the top of the form, write "Promissory Note" to clearly identify the purpose of the document.

- Enter the Date: Write the date on which the note is being created. This is important for establishing the timeline of the agreement.

- Identify the Borrower: Fill in the full name and address of the person borrowing the money. Make sure this information is accurate to avoid any confusion later.

- Identify the Lender: Next, provide the full name and address of the person or institution lending the money. This should also be precise.

- State the Loan Amount: Clearly indicate the total amount of money being borrowed for the car. This figure should be written in both numerical and written form to eliminate ambiguity.

- Specify the Interest Rate: If applicable, include the interest rate that will be charged on the loan. This could be a fixed rate or a variable rate, so clarify accordingly.

- Define the Payment Terms: Outline how and when the borrower will repay the loan. Specify the payment frequency (monthly, bi-weekly, etc.) and the duration of the loan.

- Include Late Fees: If there are any penalties for late payments, detail those here. This helps set expectations for both parties.

- Signatures: Finally, both the borrower and lender should sign the document. This signifies that both parties agree to the terms laid out in the note.

Key takeaways

When filling out and using the Promissory Note for a Car form, keep these key takeaways in mind:

- Understand the Terms: Make sure you clearly understand the loan terms, including the interest rate and payment schedule. This will help you avoid any surprises later.

- Fill it Out Accurately: Provide accurate information about the borrower and the lender. Double-check names, addresses, and the amount being financed.

- Signatures Matter: Both parties must sign the document. Without signatures, the note may not be legally binding.

- Keep a Copy: After filling it out, keep a copy for your records. This will be important for tracking payments and resolving any disputes.

Common mistakes

When individuals set out to fill out a Promissory Note for a car, they often overlook crucial details that can lead to significant complications down the line. One common mistake is failing to clearly state the loan amount. If the amount is ambiguous or incorrectly written, it can create confusion and disputes between the lender and borrower. Always double-check that the figure is correct and clearly legible.

Another frequent error involves neglecting to include the interest rate. Without this critical piece of information, the borrower may not understand the total cost of the loan over time. This omission can lead to misunderstandings and potential legal issues if the borrower believes they are paying less than what is actually required.

Many people also forget to specify the repayment schedule. Whether it’s monthly, bi-weekly, or another arrangement, clarity is essential. A vague repayment plan can result in missed payments, which may trigger penalties or damage the borrower’s credit score.

In addition, individuals sometimes fail to include the due date for the final payment. This date serves as a crucial milestone for both parties. Without it, the borrower might not know when their obligations end, leading to unnecessary stress and confusion.

Another mistake is not providing a detailed description of the car being financed. Information such as the make, model, year, and Vehicle Identification Number (VIN) should be included. This specificity protects both the lender and borrower by ensuring that there is no ambiguity about what is being financed.

People may also overlook the importance of signatures. Both parties must sign the document to validate the agreement. An unsigned note can be deemed unenforceable, leaving the lender without recourse if the borrower defaults.

Moreover, individuals often fail to consider the consequences of default. A well-drafted Promissory Note should outline what happens if the borrower cannot make payments. This could include late fees, repossession of the vehicle, or other legal actions. Clarity in this area can help prevent future disputes.

Another common oversight is not keeping a copy of the signed Promissory Note. After the agreement is executed, both parties should retain a copy for their records. This ensures that there is a reference point in case any issues arise later.

Lastly, many people underestimate the importance of seeking legal advice. While it may seem straightforward, a Promissory Note is a legally binding document. Consulting with a legal professional can help identify potential pitfalls and ensure that the note is comprehensive and enforceable.

Documents used along the form

When financing a vehicle, several documents are typically used alongside the Promissory Note for a Car. Each document serves a specific purpose in the transaction, ensuring clarity and legal protection for all parties involved.

- Bill of Sale: This document serves as proof of the transaction between the buyer and seller. It outlines the details of the sale, including the vehicle's make, model, VIN, and sale price.

- Title Transfer Document: This form is necessary to officially transfer ownership of the vehicle from the seller to the buyer. It includes information about both parties and must be filed with the relevant state authority.

- Promissory Note: This essential document outlines the borrower's commitment to repay the loan amount for the vehicle. It serves as a formal agreement, ensuring both parties understand the repayment terms and conditions, similar to the importance of templates available at NY Templates.

- Loan Agreement: If financing is involved, this document details the terms of the loan, including the interest rate, repayment schedule, and any fees associated with the loan.

- Disclosure Statement: This statement provides important information about the vehicle's condition, history, and any warranties. It ensures the buyer is fully informed before completing the purchase.

- Odometer Disclosure Statement: Required by federal law, this document verifies the vehicle's mileage at the time of sale. It helps prevent odometer fraud and ensures transparency in the transaction.

- Insurance Verification: This document proves that the buyer has obtained the necessary insurance coverage for the vehicle. It is often required by lenders before finalizing the sale.

- Power of Attorney: In some cases, this document allows one party to act on behalf of another in the transaction. It may be used if the seller is unable to be present during the sale.

These documents collectively support the vehicle purchase process, ensuring that all parties understand their rights and obligations. Properly completing and retaining these forms can help avoid potential disputes in the future.

More Promissory Note for a Car Templates:

Release of Promissory Note Template - Can be part of a larger settlement agreement in litigation cases.

A Promissory Note in Arkansas is a written promise to pay a specified amount of money to a designated person or entity at a defined time. This legal document outlines the terms of the loan, including interest rates and repayment schedules, providing clarity and security for both the lender and borrower. For those looking to understand the template better, you can find additional information and a form at https://promissoryform.com/blank-arkansas-promissory-note. Ready to create your own Promissory Note? Fill out the form by clicking the button below.

Frequently Asked Questions

What is a Promissory Note for a Car?

A Promissory Note for a Car is a written agreement between a borrower and a lender. It outlines the terms of a loan used to purchase a vehicle. This document serves as a promise from the borrower to repay the loan under specified conditions, including the amount borrowed, interest rate, repayment schedule, and any penalties for late payments.

Who needs a Promissory Note for a Car?

Anyone who is financing a vehicle purchase through a loan may need a Promissory Note. This includes:

- Individuals buying a car from a private seller.

- Buyers obtaining a loan from a bank or credit union.

- People entering into a financing agreement with a dealership.

Having a Promissory Note protects both the lender and the borrower by clearly defining the terms of the loan.

What should be included in the Promissory Note for a Car?

The Promissory Note should include essential details such as:

- The names and addresses of both the borrower and lender.

- The amount of the loan.

- The interest rate, if applicable.

- The repayment schedule, including due dates.

- Any late fees or penalties for missed payments.

- Signatures of both parties to validate the agreement.

Including these elements helps ensure clarity and can prevent disputes in the future.

What happens if the borrower fails to repay the loan?

If the borrower does not repay the loan as agreed, several consequences may occur. The lender can:

- Charge late fees as specified in the Promissory Note.

- Report the missed payments to credit bureaus, which can affect the borrower’s credit score.

- Initiate legal action to recover the owed amount.

- Repossess the vehicle, depending on the terms of the agreement.

It is crucial for borrowers to understand their obligations and communicate with the lender if they encounter financial difficulties.