Fill in a Valid Profit And Loss Template

Understanding the Profit and Loss form is essential for anyone looking to gain insights into a business's financial health. This document provides a snapshot of a company's revenues and expenses over a specific period, typically a month, quarter, or year. By analyzing this form, business owners can identify trends in income and spending, allowing them to make informed decisions about budgeting and future investments. Key components of the Profit and Loss form include total revenue, which reflects all income generated from sales, as well as various expense categories, such as cost of goods sold, operating expenses, and taxes. The bottom line, often referred to as net profit or loss, reveals whether the business is thriving or struggling financially. Additionally, the Profit and Loss form can serve as a valuable tool for attracting investors or securing loans, as it demonstrates a company’s ability to manage its finances effectively. Understanding how to read and interpret this document can empower business owners to drive their enterprises toward success.

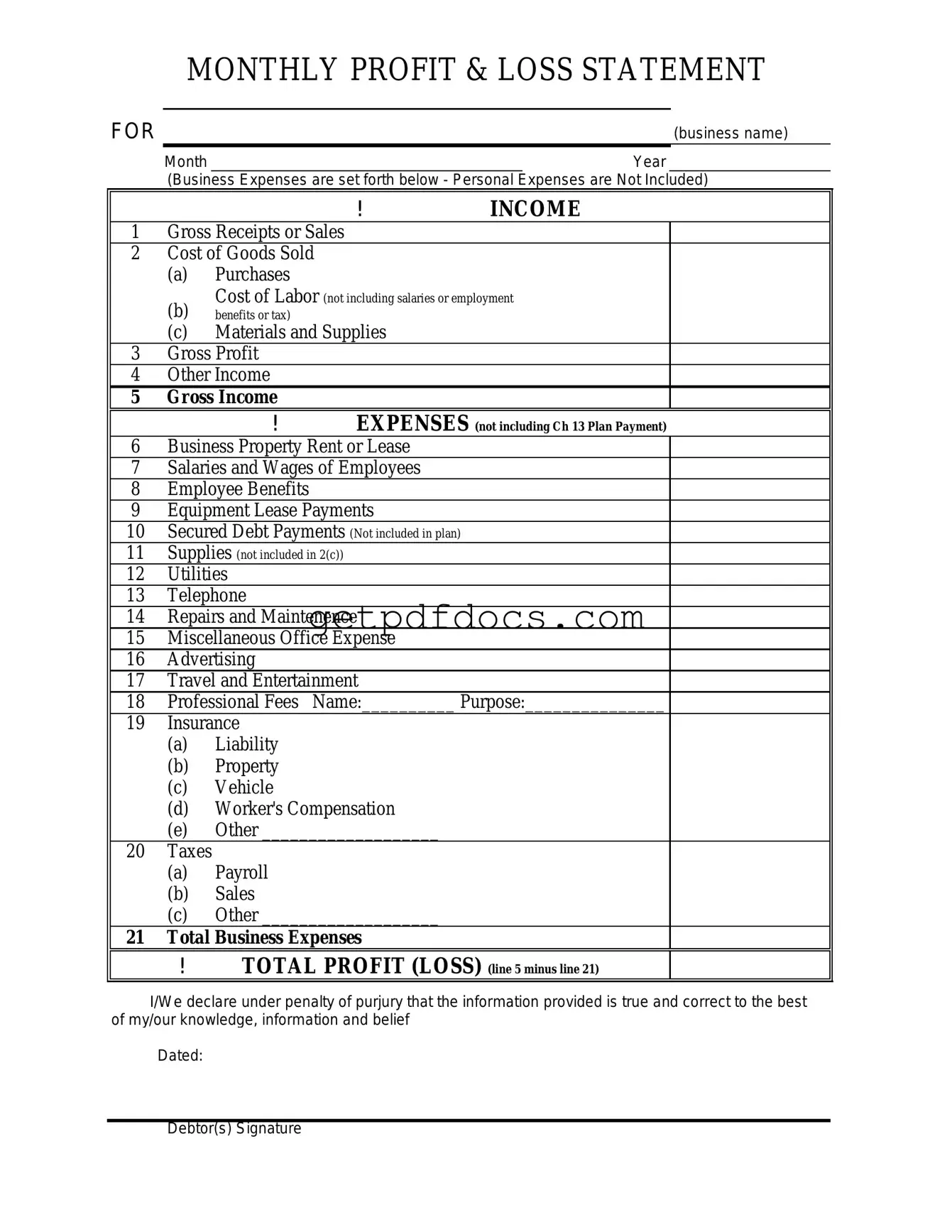

How to Use Profit And Loss

Filling out the Profit and Loss form is an important step in understanding your financial performance. Once you gather the necessary information, you can accurately complete the form, which will help you track income and expenses over a specific period. Follow these steps to ensure you fill it out correctly.

- Start with the header section. Enter your business name, the reporting period, and any other required identifiers.

- List all sources of income. Include sales revenue, service income, and any other earnings. Make sure to be thorough.

- Calculate the total income. Add up all the income sources you listed in the previous step.

- Move on to expenses. Begin listing all costs associated with running your business, such as rent, utilities, salaries, and supplies.

- Sum up all expenses. This total will give you a clear picture of your outflows during the reporting period.

- Subtract total expenses from total income. This calculation will help you determine your net profit or loss.

- Review the completed form for accuracy. Ensure all figures are correct and that you haven’t missed any income or expenses.

- Save or print the form for your records. Keeping a copy is essential for future reference and tax purposes.

Key takeaways

When filling out and using the Profit and Loss form, there are several important aspects to consider. These takeaways can help ensure accuracy and effectiveness in financial reporting.

- Understand the purpose of the Profit and Loss form. It summarizes revenues, costs, and expenses over a specific period, providing insight into business profitability.

- Gather all necessary financial documents before starting. This includes invoices, receipts, and bank statements to ensure all data is accurate and complete.

- Clearly categorize income and expenses. Use specific labels for each category to enhance clarity and facilitate analysis.

- Keep track of all revenue streams. This includes sales, service income, and any other sources of revenue to provide a comprehensive view of financial performance.

- Regularly update the form. This should be done monthly or quarterly to reflect the most current financial situation and to aid in timely decision-making.

- Review and analyze the results. Look for trends in income and expenses to identify areas for improvement or potential growth.

- Use the Profit and Loss form as a tool for strategic planning. It can help in budgeting and forecasting future financial performance.

- Consult with a financial advisor if needed. They can provide guidance on best practices for filling out the form and interpreting the results.

Common mistakes

Filling out a Profit and Loss form can be tricky. Many people make mistakes that can lead to inaccurate financial reporting. One common error is not keeping track of all income sources. When individuals or businesses overlook certain income streams, they miss out on a complete picture of their financial health. Every dollar counts, and it's crucial to account for every source of revenue.

Another frequent mistake is failing to categorize expenses correctly. Some people lump all expenses together, which can lead to confusion later on. By categorizing expenses—such as rent, utilities, and payroll—individuals can better analyze where their money goes. This clarity helps in making informed financial decisions.

Additionally, some individuals forget to update their Profit and Loss forms regularly. Relying on outdated information can skew results and lead to poor financial choices. Keeping the form current allows for a more accurate assessment of financial performance over time. Regular updates ensure that you are always working with the most relevant data.

Lastly, many people neglect to review their Profit and Loss form for errors before submission. Simple mistakes, like typos or incorrect figures, can significantly impact the results. Taking the time to double-check entries can prevent costly errors and ensure that the financial report accurately reflects the business's performance.

Documents used along the form

The Profit and Loss form is a crucial document for understanding a business's financial performance over a specific period. However, it is often used in conjunction with other forms and documents that provide a more comprehensive view of a company’s financial health. Below is a list of essential documents that complement the Profit and Loss form.

- Balance Sheet: This document provides a snapshot of a company's assets, liabilities, and equity at a specific point in time. It helps stakeholders assess the company's financial stability and liquidity.

- Cash Flow Statement: This statement outlines the cash inflows and outflows over a period. It highlights how well a company generates cash to fund its operations and pay its debts.

- Income Tax Return: This document details a company's income, expenses, and tax obligations for a given year. It is essential for compliance and provides insights into the company’s overall financial standing.

- Quitclaim Deed: When transferring property ownership in Florida, access the comprehensive Quitclaim Deed form guide to ensure all legal requirements are met.

- Budget Report: A budget report compares projected revenues and expenses to actual figures. It helps management track performance and make informed financial decisions.

- Accounts Receivable Aging Report: This report shows the outstanding invoices owed to a company, categorized by the length of time an invoice has been outstanding. It is vital for managing cash flow and collections.

- Accounts Payable Aging Report: Similar to the accounts receivable aging report, this document tracks what a company owes to its suppliers and creditors. It helps manage cash outflows and maintain good supplier relationships.

- Sales Report: This report summarizes sales data over a specific period, providing insights into revenue trends and sales performance. It is crucial for evaluating marketing strategies and business growth.

Each of these documents plays a significant role in painting a full picture of a business's financial landscape. Together, they provide valuable insights that can inform strategic decisions and help ensure long-term success.

More PDF Forms

American Automobile Association - The application’s completion assesses the applicant’s readiness for international driving.

The California Employment Verification form is a crucial document used to confirm an individual's employment status and details. This form is often required for various purposes, such as loan applications or rental agreements. To find useful resources for completing this form, you can visit California Templates, which can help streamline your verification process and ensure accuracy.

What Is Recorded on a Medicine Label Uk - The form includes the name of the medication prescribed.

Spanish Job Application - Detail your work experience, starting with the most recent job.

Frequently Asked Questions

What is a Profit and Loss form?

A Profit and Loss form, often referred to as a P&L statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period, typically a fiscal quarter or year. This form provides a clear picture of a business's profitability, helping owners and stakeholders make informed decisions. By detailing income and expenditures, it allows you to assess whether your business is operating at a profit or a loss.

Why is a Profit and Loss form important?

The Profit and Loss form is crucial for several reasons:

- Financial Insight: It offers insights into how well your business is performing financially.

- Budgeting: By analyzing past performance, you can create more accurate budgets for the future.

- Investor Relations: Investors often require P&L statements to evaluate potential returns on investment.

- Tax Preparation: This form is essential when preparing your taxes, as it provides a clear record of income and expenses.

How often should I prepare a Profit and Loss form?

The frequency of preparing a Profit and Loss form depends on the nature of your business and your financial needs. Many businesses prepare these statements monthly or quarterly to closely monitor performance and make timely adjustments. However, at a minimum, you should prepare an annual P&L statement to satisfy tax requirements and assess overall business health.

What are the key components of a Profit and Loss form?

A standard Profit and Loss form includes several key components:

- Revenue: Total income generated from sales or services.

- Cost of Goods Sold (COGS): Direct costs associated with the production of goods sold.

- Gross Profit: Revenue minus COGS, showing the profit before operating expenses.

- Operating Expenses: Costs incurred in the normal course of business, such as rent, utilities, and salaries.

- Net Profit or Loss: The final figure after subtracting all expenses from total revenue, indicating overall profitability.

Can I create a Profit and Loss form myself?

Yes, you can create a Profit and Loss form yourself. Many templates are available online, making it easy to get started. You can use spreadsheet software like Microsoft Excel or Google Sheets to customize your form. Just ensure that you accurately track all income and expenses throughout the period you are analyzing. However, if you feel overwhelmed, consider consulting with a financial professional to ensure accuracy and compliance with accounting standards.