Fill in a Valid Mortgage Statement Template

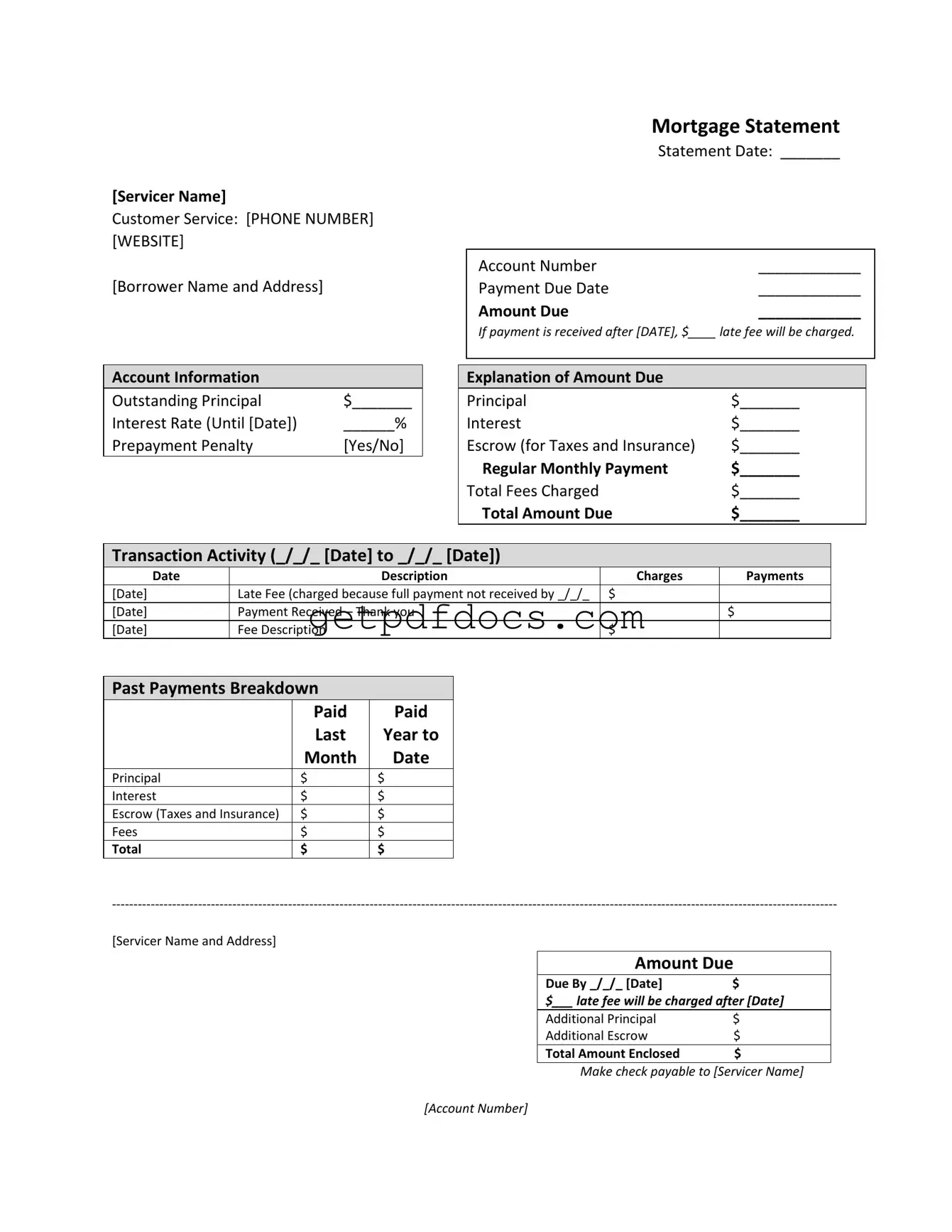

The Mortgage Statement form serves as a crucial document for homeowners, providing a comprehensive overview of their mortgage account. At the top, the form identifies the servicer’s name, customer service contact details, and the borrower’s information, ensuring that recipients know whom to contact for questions. The statement date, account number, payment due date, and total amount due are prominently displayed, along with a warning about potential late fees if payments are not received on time. Essential account information follows, detailing the outstanding principal, interest rate, and whether a prepayment penalty applies. A breakdown of the amount due clarifies how much of the payment goes toward principal, interest, and escrow for taxes and insurance. Additionally, the transaction activity section provides a timeline of recent payments and charges, offering transparency about the account’s status. The form also includes important messages about partial payments and potential consequences of delinquency, emphasizing the importance of timely payments to avoid fees and foreclosure. Lastly, resources for financial assistance are highlighted, ensuring that borrowers are aware of options available to them in times of financial difficulty.

How to Use Mortgage Statement

Completing the Mortgage Statement form is an important step in managing your mortgage. This form provides essential information about your account, including payment details and outstanding balances. Follow these steps to fill out the form accurately.

- Begin with the Servicer Name section. Write the name of your mortgage servicer.

- In the Customer Service section, include the phone number and website for customer inquiries.

- Fill in your Borrower Name and Address at the designated space.

- For the Statement Date, write the date you are filling out the form.

- Enter your Account Number in the provided field.

- Write the Payment Due Date in the appropriate spot.

- In the Amount Due section, fill in the total amount you owe.

- Note the date after which a late fee will be charged and write the fee amount.

- In the Account Information section, list the Outstanding Principal amount.

- Fill in the Interest Rate and the date it is valid until.

- Indicate if there is a Prepayment Penalty by writing "Yes" or "No."

- In the Explanation of Amount Due section, break down the amounts for Principal, Interest, Escrow, Regular Monthly Payment, Total Fees Charged, and Total Amount Due.

- For the Transaction Activity, list the date range and provide details for each transaction, including charges and payments.

- In the Past Payments Breakdown section, fill in the amounts paid for Principal, Interest, Escrow, Fees, and the Total for the last year.

- Write the Amount Due and the Due By date at the bottom of the form.

- Include any additional amounts for Principal and Escrow, if applicable.

- Calculate the Total Amount Enclosed and write that amount.

- Make your check payable to the Servicer Name and include your Account Number on it.

Once you have filled out the form, review it for accuracy. Ensure that all amounts are correct and that your contact information is up to date. After confirming everything is in order, you can submit the form as instructed.

Key takeaways

When it comes to filling out and using the Mortgage Statement form, here are some key takeaways to keep in mind:

- Check Your Information: Ensure that your name, address, and account number are correct. Mistakes can lead to confusion.

- Understand the Amount Due: The form clearly outlines the total amount due, including principal, interest, and any fees. Make sure to review this carefully.

- Payment Due Date: Pay attention to the payment due date. If you miss this date, a late fee will be charged.

- Partial Payments: Remember that partial payments are held in a suspense account and do not apply to your mortgage until the full amount is paid.

- Delinquency Notice: If you are late on payments, the form will indicate how many days you are delinquent. This is important to address promptly.

- Recent Account History: Review your recent account history section. It shows your payment patterns and any unpaid balances.

- Seek Help if Needed: If you are experiencing financial difficulty, the form provides information about mortgage counseling and assistance.

Using this form effectively can help you stay on top of your mortgage and avoid potential issues. Always keep a copy for your records.

Common mistakes

Filling out the Mortgage Statement form can be a straightforward task, but there are common mistakes that can complicate the process. One of the most frequent errors is failing to include accurate personal information. When entering your borrower name and address, ensure that every detail matches official documents. Any discrepancies may lead to delays in processing your payment or even miscommunication with your mortgage servicer.

Another common mistake is neglecting to check the statement date and the payment due date. It’s essential to fill in these dates correctly, as they determine when your payment is due and when late fees may apply. Missing or incorrect dates can lead to unnecessary late fees, which can add financial strain.

Many people also overlook the importance of detailing the amount due. This figure should reflect the total of all components, including principal, interest, and any escrow amounts. Failing to calculate this correctly can result in underpayment or overpayment, complicating your financial situation.

In addition, individuals often forget to note the account number. This number is crucial for ensuring that payments are credited to the correct account. Without it, your payment may be misallocated, leading to further complications down the line.

Another frequent error is not understanding the implications of partial payments. If you make a partial payment, it will not be applied to your mortgage but will instead be held in a suspense account. This can create confusion and potentially lead to further delinquency if not managed properly.

Additionally, many individuals fail to review the transaction activity section thoroughly. This area provides a history of charges and payments, which can help you understand your account status. Ignoring this section might result in missing out on important information regarding late fees or previous payments.

Some borrowers also neglect to include a check or payment method when submitting the form. It is vital to ensure that the total amount enclosed is accurate and that the check is made payable to the correct servicer. Omitting this step can lead to delays in processing your payment.

Finally, it’s essential to pay attention to the delinquency notice included in the form. If you are behind on payments, the notice provides critical information regarding your account status and the potential consequences of continued delinquency. Ignoring this notice can lead to severe repercussions, including foreclosure.

Documents used along the form

When managing a mortgage, several documents accompany the Mortgage Statement form to provide a comprehensive view of the loan and its status. Understanding these documents can help borrowers stay informed about their mortgage obligations and any potential issues that may arise.

- Loan Agreement: This is the original contract between the borrower and the lender. It outlines the terms of the mortgage, including the loan amount, interest rate, repayment schedule, and any penalties for late payments. It serves as the foundational document for the mortgage.

- Amortization Schedule: This document breaks down each payment over the life of the loan. It details how much of each payment goes toward the principal and how much goes toward interest. Borrowers can see how their loan balance decreases over time.

- Dog Bill of Sale: This legal document records the transfer of ownership of a dog from one party to another. It serves as proof of sale, including essential details about the dog, such as breed, age, and any health information. If you’re looking to buy or sell a dog in California, consider filling out this important form by clicking California Templates.

- Escrow Account Statement: If the mortgage includes an escrow account for property taxes and insurance, this statement provides information about the funds held in escrow. It shows the amounts collected and disbursed, helping borrowers understand their total housing costs.

- Payment History: This document records all payments made on the mortgage. It includes dates, amounts, and whether payments were made on time. A clear payment history can help borrowers track their payment patterns and identify any issues.

- Delinquency Notice: If payments are missed, this notice alerts the borrower to their delinquent status. It outlines the consequences of continued non-payment, including potential fees and foreclosure risks. This document is crucial for borrowers to understand the urgency of addressing missed payments.

Being familiar with these documents can empower borrowers to manage their mortgages more effectively. Each piece of information contributes to a clearer picture of the loan, helping individuals make informed decisions about their financial future.

More PDF Forms

Florida Real Estate Forms - The responsibilities for property operations during the contract period are outlined.

Test Drive Form Pdf - Take the opportunity to assess vehicle comfort and handling.

For parents looking to make informed decisions regarding their child's welfare, the process of handling a Power of Attorney for a Child can be straightforward. Ensure you understand the implications of this legal document by reviewing our guide on the important aspects of the Power of Attorney for a Child.

How to Get Paystubs - It's important for employees to keep pay stubs for their records.

Frequently Asked Questions

What is a Mortgage Statement?

A Mortgage Statement is a document that provides a summary of your mortgage account. It includes important details such as your outstanding balance, payment history, and any fees that may apply. This statement is typically sent monthly by your mortgage servicer.

What information can I find on my Mortgage Statement?

Your Mortgage Statement includes several key pieces of information:

- Account number

- Outstanding principal balance

- Interest rate

- Payment due date and amount

- Transaction activity

- Past payments breakdown

This information helps you keep track of your mortgage and manage your payments effectively.

How do I read the Amount Due section?

The Amount Due section breaks down what you owe into different categories:

- Principal: The amount you borrowed

- Interest: The cost of borrowing

- Escrow: Funds set aside for taxes and insurance

- Total Fees Charged: Any additional fees incurred

Adding these amounts together gives you the total amount due for that billing period.

What happens if I miss a payment?

If you miss a payment, a late fee will be charged as indicated on your statement. It’s crucial to pay your mortgage on time to avoid additional fees and potential negative impacts on your credit score.

What is a partial payment?

A partial payment is any amount less than your total monthly payment. If you make a partial payment, it won’t be applied to your mortgage balance immediately. Instead, it will be held in a separate suspense account until you pay the full amount.

What does it mean if I see a delinquency notice?

A delinquency notice indicates that you are behind on your mortgage payments. It’s essential to address this situation promptly, as continued delinquency may lead to fees or even foreclosure, which is the loss of your home.

How can I bring my mortgage current if I’m behind?

To bring your mortgage current, you need to pay the total amount due as stated on your Mortgage Statement. This includes any past due amounts and late fees. Contact your servicer if you need assistance or have questions about your payment options.

What should I do if I’m experiencing financial difficulty?

If you’re facing financial challenges, it’s important to reach out for help. Your Mortgage Statement may provide information on mortgage counseling services. These resources can assist you in finding solutions to manage your payments and avoid foreclosure.

Who should I contact for questions about my Mortgage Statement?

If you have questions or need clarification about your Mortgage Statement, contact your mortgage servicer’s customer service. The contact information is usually listed on the statement, including a phone number and website for further assistance.