Attorney-Approved Promissory Note Form for Michigan State

The Michigan Promissory Note form serves as a crucial financial document that outlines the terms of a loan agreement between a borrower and a lender. This legally binding instrument specifies the amount borrowed, the interest rate applicable, and the repayment schedule, ensuring clarity and mutual understanding between the parties involved. It often includes details about late fees, prepayment options, and the consequences of default, which provide additional security for the lender. Furthermore, the form may require signatures from both parties to validate the agreement, emphasizing the importance of consent and acknowledgment in financial transactions. By adhering to the established guidelines, individuals can protect their rights and responsibilities, fostering trust and transparency in lending practices. Whether used for personal loans, business financing, or other purposes, the Michigan Promissory Note form plays a vital role in facilitating responsible borrowing and lending within the state.

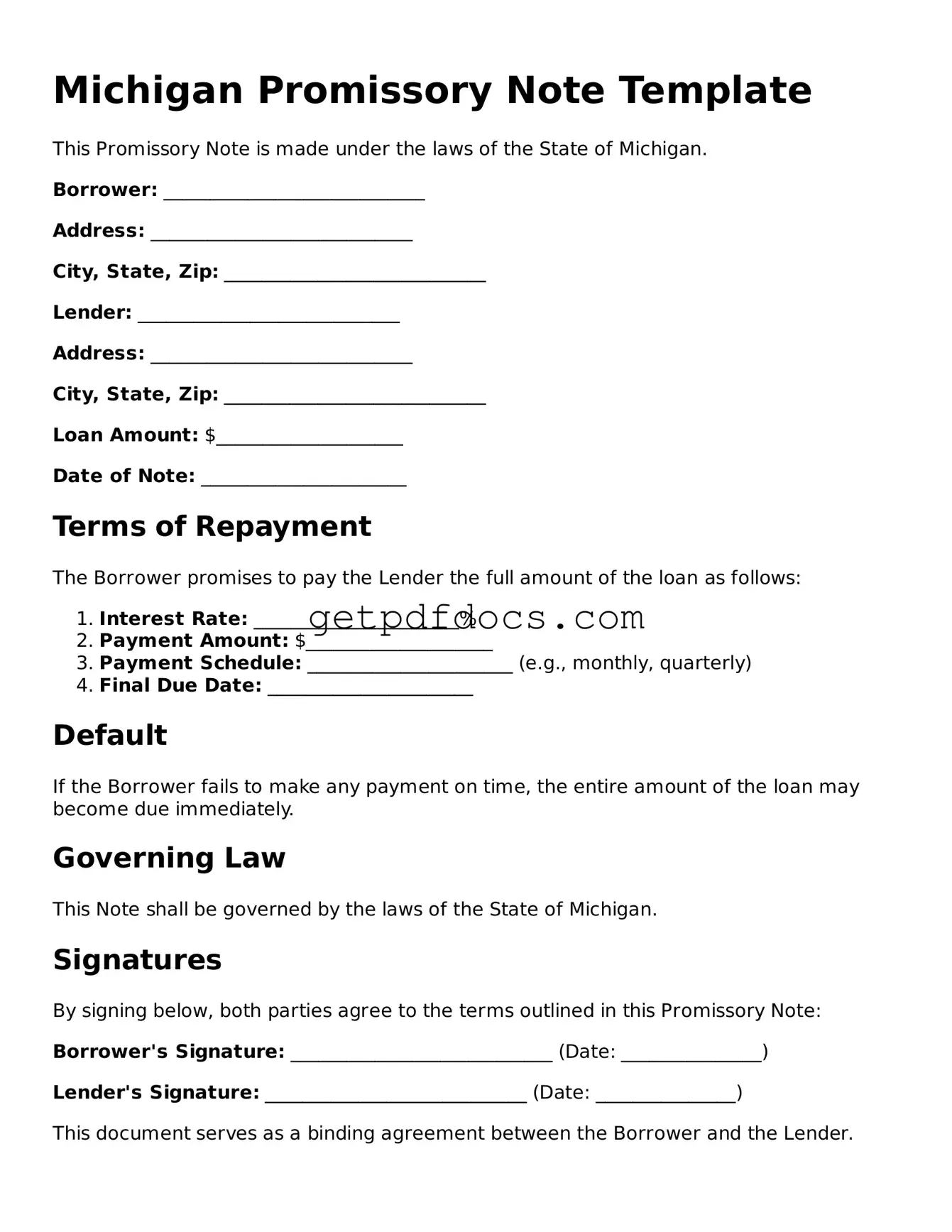

How to Use Michigan Promissory Note

After obtaining the Michigan Promissory Note form, you are ready to fill it out. This process requires attention to detail to ensure that all necessary information is correctly entered. Follow the steps below to complete the form accurately.

- Begin by entering the date at the top of the form. Use the format MM/DD/YYYY.

- Fill in the name and address of the borrower. This should include the full name and current residential address.

- Next, enter the name and address of the lender. Ensure that the lender's information is complete and accurate.

- Specify the principal amount being borrowed. This is the total sum that the borrower is agreeing to repay.

- Indicate the interest rate. Write the percentage clearly, as it affects the total amount owed.

- Detail the repayment schedule. Include when payments are due and how often they will occur (monthly, quarterly, etc.).

- Provide any additional terms or conditions that may apply to the loan. Be specific to avoid confusion later.

- Have the borrower sign and date the form. This signature indicates their agreement to the terms outlined.

- If required, have a witness or notary public sign the document as well. This adds an extra layer of verification.

Once you have completed these steps, review the form for accuracy. Make sure all information is clear and legible. After that, keep a copy for your records and provide the original to the lender.

Key takeaways

When filling out and using the Michigan Promissory Note form, there are several important points to keep in mind. Below are key takeaways that can help ensure the process is clear and effective.

- The promissory note serves as a written promise to repay a loan, detailing the amount borrowed and the terms of repayment.

- It is essential to include the names and addresses of both the borrower and the lender to establish clear identification of the parties involved.

- The note should specify the interest rate, if applicable, and the repayment schedule, including due dates and any grace periods.

- Both parties should sign and date the document to indicate their agreement to the terms outlined in the note.

- Keep a copy of the signed promissory note for personal records, as it serves as a legal document in case of disputes or misunderstandings.

Common mistakes

Filling out a Michigan Promissory Note form can seem straightforward, but many individuals make common mistakes that can lead to complications down the road. Understanding these pitfalls can help ensure that the document serves its intended purpose effectively. One frequent error is neglecting to include the full names of both the borrower and the lender. This may seem minor, but without clear identification, the note can become ambiguous, making it difficult to enforce later.

Another common mistake involves the omission of the date. A promissory note should always include the date it is signed. This date is crucial, as it establishes the timeline for repayment and can affect interest calculations. Additionally, failing to specify the loan amount clearly can lead to misunderstandings. It’s essential to write out the amount in both numeric and word form to eliminate any confusion.

Many people also overlook the importance of detailing the repayment terms. Whether the borrower will make monthly payments, a lump sum payment, or follow a different schedule, clarity is key. Vague terms can result in disputes. Furthermore, forgetting to include the interest rate is another frequent error. Without this information, the lender may find it challenging to enforce the terms of the loan.

Another mistake involves neglecting to include any late fees or penalties for missed payments. Clearly stating these terms can provide both parties with a sense of security and understanding. Some individuals also fail to sign the document. A promissory note is not legally binding without the signatures of both parties, so this step is crucial.

It’s important to remember that witnesses or notarization may be required in certain situations. Skipping this step can render the note less enforceable. Additionally, people often forget to keep copies of the signed document for their records. Having a copy can be invaluable if disputes arise later.

Lastly, failing to review the entire document for accuracy before submission can lead to errors that are easily avoidable. Taking the time to double-check every detail ensures that the promissory note is not only valid but also serves the interests of both parties effectively. By being mindful of these common mistakes, individuals can navigate the process of creating a Michigan Promissory Note with confidence and clarity.

Documents used along the form

When dealing with a Michigan Promissory Note, several additional forms and documents may be necessary to ensure clarity and legal compliance. These documents help outline the terms of the loan, provide security for the lender, and establish the rights and responsibilities of both parties involved. Below is a list of commonly used documents that accompany a Promissory Note.

- Loan Agreement: This document outlines the terms of the loan, including interest rates, repayment schedules, and any fees associated with the loan. It serves as a comprehensive agreement between the lender and borrower.

- Security Agreement: If the loan is secured by collateral, this agreement details the collateral involved. It protects the lender's interests in case the borrower defaults on the loan.

- Disclosure Statement: This document provides essential information about the loan, including total costs, interest rates, and any potential penalties. It ensures that the borrower understands the financial implications of the loan.

- Personal Guarantee: If a business is borrowing, a personal guarantee may be required from the business owner. This document holds the owner personally liable for the loan if the business fails to repay.

- Amortization Schedule: This schedule breaks down the repayment plan into specific payments over time. It shows how much of each payment goes toward interest and principal.

- Payment Receipt: After each payment is made, a receipt should be issued. This document serves as proof of payment and can be important for record-keeping.

- Default Notice: In the event of a missed payment, this notice informs the borrower of the default. It outlines the consequences and steps the borrower must take to remedy the situation.

- Dirt Bike Bill of Sale: This essential document is instrumental in transferring ownership of dirt bikes and can be obtained from California Templates.

- Release of Liability: Once the loan is fully repaid, this document releases the borrower from any further obligations. It confirms that the lender has no claim against the borrower regarding the loan.

Each of these documents plays a crucial role in the lending process. They help protect both the lender and the borrower by clearly defining expectations and responsibilities. Always consider consulting with a legal professional to ensure that all necessary documents are properly prepared and executed.

Browse Other Common Promissory Note Forms for Different States

California Promissory Note - A promissory note outlines the terms of repayment, including interest rates and payment schedules.

Free Promissory Note Template Florida - The lender can pursue collections if the borrower does not fulfill the payment obligations.

For those considering the legal implications of child care, understanding the Power of Attorney for a Child form is crucial. This document grants a trusted individual the authority to make important decisions regarding your child's welfare in various scenarios.

Promissory Note Washington State - Borrowers should read the terms carefully before signing a promissory note.

Frequently Asked Questions

What is a Michigan Promissory Note?

A Michigan Promissory Note is a legal document in which one party (the borrower) agrees to repay a specific amount of money to another party (the lender) under agreed-upon terms. This note outlines important details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. It serves as a formal acknowledgment of the debt and provides protection for both parties involved.

What are the key components of a Michigan Promissory Note?

Several essential elements should be included in a Michigan Promissory Note:

- Parties Involved: Clearly identify the borrower and lender by name and address.

- Loan Amount: Specify the total amount of money being borrowed.

- Interest Rate: Indicate the interest rate, if applicable, and whether it is fixed or variable.

- Repayment Terms: Outline the repayment schedule, including due dates and payment amounts.

- Default Terms: Include any conditions that would constitute a default and the consequences of defaulting.

Do I need to have the Promissory Note notarized?

While notarization is not strictly required for a Michigan Promissory Note to be valid, it is highly recommended. Having the document notarized adds an extra layer of authenticity and can help prevent disputes regarding the agreement. A notary public verifies the identities of the parties involved and confirms that they are signing voluntarily.

Can a Michigan Promissory Note be modified after it has been signed?

Yes, a Michigan Promissory Note can be modified after it has been signed, but both parties must agree to the changes. It is advisable to document any modifications in writing, and ideally, have them signed and dated by both parties. This ensures that the new terms are clear and legally enforceable.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults on the Promissory Note, the lender has several options. Typically, the lender may choose to:

- Charge late fees as outlined in the note.

- Initiate collection proceedings to recover the owed amount.

- Take legal action, which may result in a court judgment against the borrower.

It's crucial for both parties to understand the consequences of defaulting and to communicate openly to avoid escalation of the situation.