Printable Loan Agreement Template

When entering into a loan agreement, it is essential to understand the key components that make up this important document. A loan agreement serves as a formal contract between a lender and a borrower, outlining the terms and conditions of the loan. This includes critical details such as the loan amount, interest rate, repayment schedule, and any applicable fees. Furthermore, the agreement specifies the consequences of defaulting on the loan, ensuring that both parties are aware of their rights and responsibilities. Additional elements may include collateral requirements, prepayment options, and any covenants that the borrower must adhere to during the loan term. By carefully reviewing these aspects, individuals can protect their interests and ensure a clear understanding of the financial arrangement they are entering into.

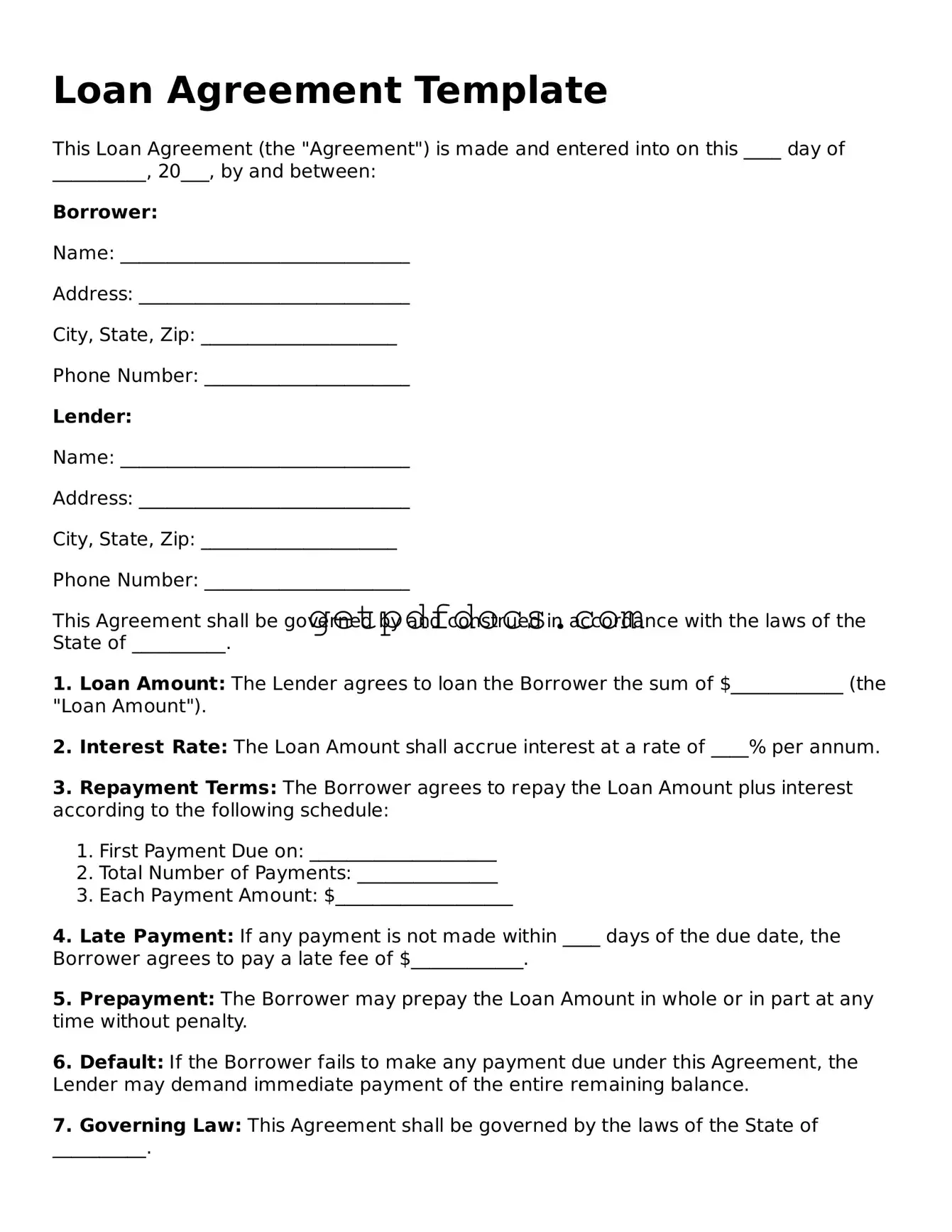

How to Use Loan Agreement

After obtaining the Loan Agreement form, follow these steps to complete it accurately. Ensure that you have all necessary information ready before you start filling out the form.

- Begin with the borrower's full name. Write it in the designated section at the top of the form.

- Provide the borrower's address. Include street, city, state, and zip code.

- Enter the lender's name in the next section. This is the individual or institution providing the loan.

- Fill in the lender's address, similar to the borrower's address format.

- Specify the loan amount. Clearly write the total amount being borrowed.

- Indicate the interest rate. This should be a percentage and clearly stated.

- Detail the loan term. Specify the duration of the loan in months or years.

- Provide the repayment schedule. Indicate how often payments will be made (e.g., monthly, quarterly).

- Include any collateral information if applicable. Describe any assets pledged against the loan.

- Review all entries for accuracy. Ensure that all information is complete and correct.

- Sign and date the form at the bottom. The borrower must sign, and the date of signing should be noted.

Once the form is filled out, it should be submitted to the lender for review and processing. Make sure to keep a copy for your records.

Loan Agreement - Adapted for Individual States

Loan Agreement Document Subtypes

Key takeaways

When filling out and using a Loan Agreement form, there are several important considerations to keep in mind. Below are key takeaways that can help ensure the process is smooth and legally sound.

- Identify the Parties: Clearly state the names and contact information of both the lender and the borrower. This helps establish the legal relationship between the parties.

- Specify the Loan Amount: Clearly indicate the total amount being borrowed. This figure should be precise to avoid any misunderstandings.

- Detail the Interest Rate: Include the interest rate applicable to the loan. This rate can be fixed or variable, and it should comply with state usury laws.

- Outline the Repayment Terms: Specify the repayment schedule, including the frequency of payments (monthly, quarterly, etc.) and the due dates.

- Include Late Fees: If applicable, outline any late fees that will be charged if payments are not made on time. This encourages timely payments.

- State the Purpose of the Loan: Clearly define what the loan is intended for, whether it be for personal use, business expenses, or other purposes.

- Address Collateral: If the loan is secured, describe the collateral that will back the loan. This provides security for the lender.

- Include Default Terms: Clearly outline what constitutes a default and the potential consequences, such as acceleration of the loan or legal action.

- Signatures Required: Ensure that both parties sign the agreement. This signifies mutual consent and acceptance of the terms.

- Keep Copies: After signing, both parties should retain copies of the agreement for their records. This helps in case of future disputes.

By following these guidelines, both lenders and borrowers can navigate the Loan Agreement process more effectively, minimizing risks and misunderstandings.

Common mistakes

Filling out a Loan Agreement form can be a straightforward process, but many individuals make common mistakes that can lead to complications down the line. One frequent error is providing incorrect personal information. This includes misspelling names, entering the wrong Social Security number, or providing an outdated address. Such inaccuracies can delay the loan approval process and may even result in the rejection of the application.

Another mistake often seen is failing to read the terms and conditions thoroughly. Borrowers may overlook important details regarding interest rates, repayment schedules, or fees associated with the loan. This lack of attention can lead to misunderstandings about the total cost of the loan and the obligations of the borrower. It is crucial to understand what is being agreed to before signing the document.

In addition, some individuals neglect to disclose all relevant financial information. This includes income, existing debts, and other financial obligations. Providing incomplete or misleading information can jeopardize the loan application and may raise red flags for lenders. Transparency is key in building trust with the lender and ensuring a smooth approval process.

Lastly, many people forget to ask questions or seek clarification on aspects of the agreement they do not understand. It is essential to communicate with the lender about any uncertainties. Ignoring this step can lead to signing an agreement that is not fully understood, potentially resulting in unfavorable terms or conditions. Always take the time to clarify any points before proceeding.

Documents used along the form

A Loan Agreement is a key document in the lending process, outlining the terms and conditions between the borrower and the lender. Alongside this agreement, several other forms and documents are commonly used to support the transaction and ensure clarity for both parties. Below is a list of these documents.

- Promissory Note: This document serves as a written promise from the borrower to repay the loan. It includes details such as the loan amount, interest rate, and repayment schedule.

- Security Agreement: If the loan is secured, this agreement outlines the collateral that the borrower offers to the lender. It specifies the rights of the lender in case of default.

- Loan Application: The borrower typically fills out this form to provide the lender with necessary personal and financial information. This information helps the lender assess the borrower's creditworthiness.

- Dog Bill of Sale: This form is essential for documenting the sale or transfer of ownership of a dog, providing proof of the transaction and outlining important details such as buyer and seller information, the dog's description, and any health guarantees. You can find the Bill of Sale for Dogs for California to facilitate this process.

- Disclosure Statement: This document informs the borrower about the terms of the loan, including fees, interest rates, and any potential penalties. It ensures transparency in the lending process.

- Closing Statement: This statement summarizes the final terms of the loan agreement. It includes details about the disbursement of funds and any closing costs associated with the loan.

These documents work together to create a comprehensive framework for the loan process. Understanding each one can help borrowers and lenders navigate their responsibilities and rights effectively.

Other Documents

Simple Media Release Form - Use this form to confirm your approval for media presence at events you attend.

The California Employment Verification form is a crucial document used to confirm an individual's employment status and details. This form is often required for various purposes, such as loan applications or rental agreements. Understanding how to fill it out correctly can streamline your verification process, so be sure to complete the form by clicking the button below, and for further assistance, you can refer to California Templates.

How to Transfer Ownership of a Tractor - Serves as proof of ownership transfer for both buyer and seller.

Frequently Asked Questions

What is a Loan Agreement?

A Loan Agreement is a legal document that outlines the terms and conditions under which one party lends money to another. It specifies the amount borrowed, the interest rate, the repayment schedule, and any other relevant terms. This agreement protects both the lender and the borrower by clearly defining their rights and responsibilities.

Who needs a Loan Agreement?

Anyone involved in a lending situation should consider using a Loan Agreement. This includes:

- Individuals lending money to friends or family

- Businesses providing loans to employees or clients

- Financial institutions offering personal or business loans

Having a written agreement helps prevent misunderstandings and provides legal protection if disputes arise.

What should be included in a Loan Agreement?

A comprehensive Loan Agreement should include the following key elements:

- The names and addresses of the lender and borrower

- The loan amount

- The interest rate

- The repayment schedule

- Any fees or penalties for late payments

- Consequences of defaulting on the loan

- Signatures of both parties

Including these details ensures clarity and helps both parties understand their obligations.

How is interest calculated in a Loan Agreement?

Interest can be calculated in different ways, typically as a fixed rate or a variable rate. A fixed rate remains the same throughout the loan term, while a variable rate may change based on market conditions. The Loan Agreement should clearly state how interest will be calculated and when it will be applied to the outstanding balance.

Can a Loan Agreement be modified?

Yes, a Loan Agreement can be modified, but both parties must agree to the changes. It is essential to document any modifications in writing and have both parties sign the updated agreement. This ensures that the new terms are enforceable and clear to both parties.

What happens if the borrower defaults on the loan?

If the borrower defaults, the lender may take specific actions as outlined in the Loan Agreement. This could include:

- Charging late fees

- Initiating legal proceedings to recover the owed amount

- Seizing collateral, if applicable

Understanding these consequences beforehand can help both parties manage risks effectively.

Is a Loan Agreement legally binding?

Yes, a properly executed Loan Agreement is legally binding. Once both parties sign the document, they are obligated to adhere to the terms outlined. If either party fails to comply, the other party may seek legal remedies. It is advisable to keep a copy of the signed agreement for reference.

Should I consult a lawyer before signing a Loan Agreement?

While it is not always necessary to consult a lawyer, doing so can be beneficial, especially for larger loans or complex agreements. A legal professional can help ensure that the terms are fair and compliant with applicable laws. This extra step can provide peace of mind for both the lender and the borrower.