Fill in a Valid IRS 1040 Template

The IRS 1040 form serves as the cornerstone for individual income tax filing in the United States, playing a critical role in how taxpayers report their earnings and calculate their tax liabilities. This form provides a comprehensive framework for individuals to detail their income from various sources, including wages, dividends, and self-employment earnings. It allows taxpayers to claim deductions, such as those for mortgage interest, student loan interest, and charitable contributions, which can significantly reduce taxable income. Additionally, the 1040 form includes sections for reporting tax credits, which can directly lower the amount of tax owed. Understanding the nuances of the 1040 is essential for taxpayers, as it not only impacts their financial responsibilities but also influences potential refunds or additional payments. As the tax season approaches, familiarity with this form becomes increasingly important, making it vital for individuals to grasp its components and implications fully.

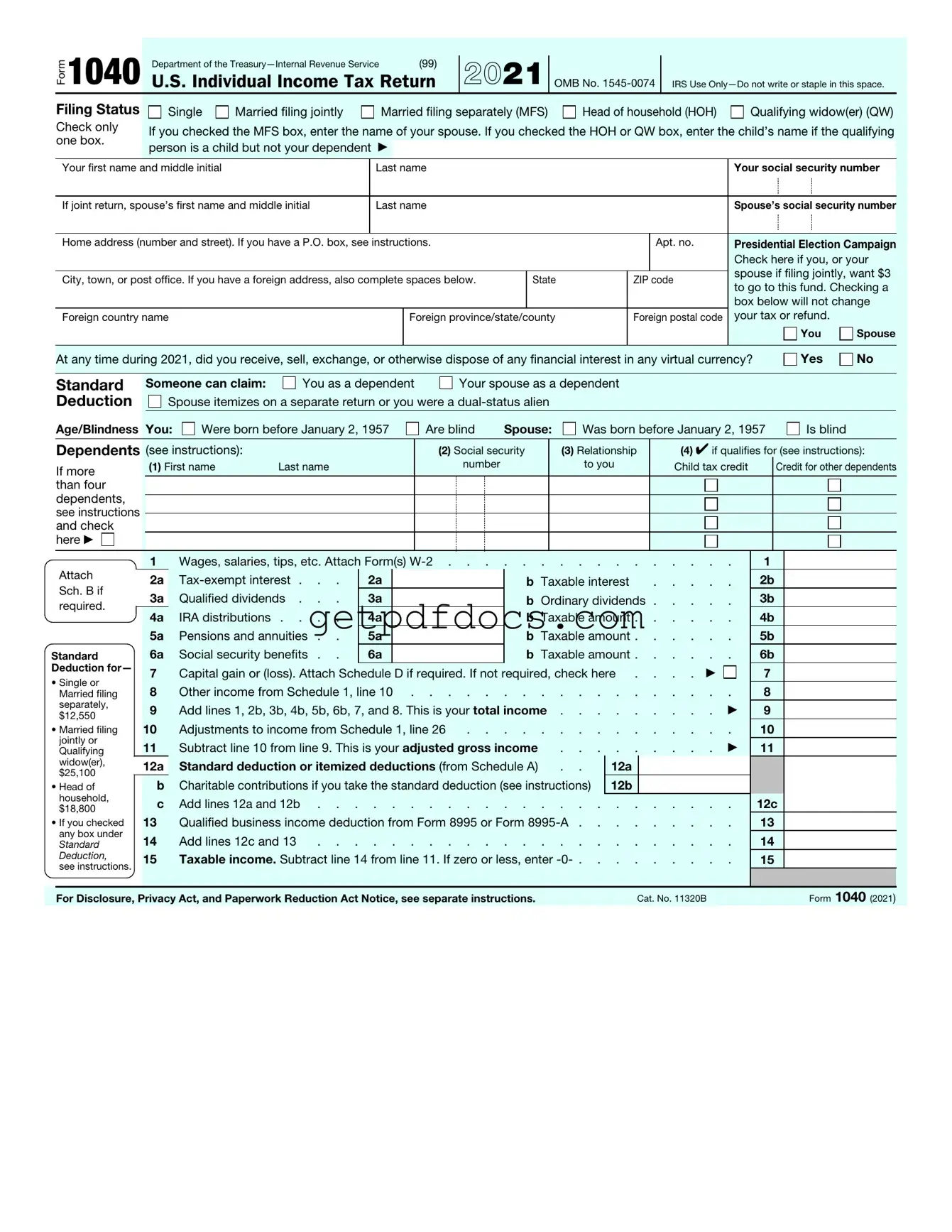

How to Use IRS 1040

Completing the IRS 1040 form is an important step in filing your annual tax return. This process involves gathering personal information, income details, and deductions. Follow these steps carefully to ensure accurate submission.

- Gather your personal information, including your name, address, and Social Security number.

- Collect income documents such as W-2s from employers and 1099 forms for other income sources.

- Begin filling out the form by entering your filing status: single, married filing jointly, married filing separately, head of household, or qualifying widow(er).

- Report your income on the appropriate lines, adding all sources together to calculate your total income.

- Determine your adjusted gross income (AGI) by subtracting any adjustments from your total income.

- Calculate your taxable income by applying the standard deduction or itemized deductions to your AGI.

- Use the tax tables provided in the instructions to find your tax liability based on your taxable income.

- Account for any tax credits you qualify for, which can reduce your overall tax bill.

- Determine your total tax owed by adding any additional taxes, if applicable.

- Subtract any payments you’ve made throughout the year, such as withholding and estimated tax payments.

- If your total payments exceed your tax owed, you will receive a refund. If not, you will need to pay the difference.

- Sign and date the form before submitting it, either electronically or via mail.

Key takeaways

When filling out and using the IRS 1040 form, consider the following key takeaways:

- Gather all necessary documents, including W-2s, 1099s, and any other income statements.

- Ensure personal information, such as Social Security numbers and addresses, is accurate and up to date.

- Choose the correct filing status, as it affects tax rates and eligibility for certain credits.

- Be aware of available deductions and credits that may reduce your taxable income.

- Double-check calculations to avoid errors that could lead to delays or penalties.

- File on time to avoid late fees and interest on any taxes owed.

Common mistakes

Filing your taxes can feel overwhelming, especially when it comes to filling out the IRS 1040 form. Many people make common mistakes that can lead to delays or even penalties. Understanding these pitfalls can help you avoid them and ensure a smoother filing process.

One of the most frequent errors occurs with personal information. It’s crucial to double-check that your name, Social Security number, and address are correct. A simple typo can lead to confusion and might delay your refund. If you’re filing jointly, make sure both names are spelled accurately and the correct Social Security numbers are listed.

Another common mistake is failing to report all income. All sources of income must be included, whether it’s from a job, freelance work, or investments. The IRS receives copies of your income statements, so omitting any earnings can raise red flags and result in penalties.

Many people also overlook deductions and credits they may be eligible for. It’s essential to research and understand what deductions can apply to your situation. For instance, expenses related to education, medical costs, or home mortgage interest could significantly reduce your taxable income. Missing out on these can mean paying more than necessary.

Inaccurate calculations are another common issue. Whether it’s simple math errors or miscalculating your tax liability, these mistakes can lead to incorrect filings. Take your time to ensure all calculations are accurate, or consider using tax software that can help minimize errors.

People often forget to sign and date their forms. This might seem minor, but without your signature, the IRS will consider your return incomplete. If you’re filing jointly, both spouses must sign the form. Don’t let this simple oversight hold up your refund.

Lastly, submitting your return late can lead to penalties and interest. The IRS expects you to file by the deadline, which is typically April 15th. If you can’t meet this deadline, it’s better to file for an extension rather than miss the deadline entirely.

By being aware of these common mistakes, you can navigate the tax filing process more effectively. Taking the time to review your 1040 form carefully will save you time, money, and potential headaches down the road.

Documents used along the form

The IRS 1040 form is a key document for individual taxpayers in the United States. However, several other forms and documents often accompany it to ensure accurate reporting of income, deductions, and credits. Below is a list of commonly used forms that may be needed alongside the 1040 form.

- W-2 Form: This form reports an employee's annual wages and the taxes withheld from their paycheck. Employers must provide this document to employees by January 31 each year.

- 1099 Form: Various versions of this form report income earned from sources other than employment, such as freelance work or interest income. Recipients must receive their 1099 forms by January 31.

- Schedule A: This form is used to itemize deductions instead of taking the standard deduction. Taxpayers can list expenses like mortgage interest, state taxes, and charitable contributions.

- Last Will and Testament Form: This important legal document allows individuals to specify how their property and affairs should be managed and distributed after their death, ensuring wishes are respected. For more information, visit https://floridaforms.net/blank-last-will-and-testament-form/.

- Schedule C: Self-employed individuals use this form to report income and expenses from their business. It helps calculate the net profit or loss for the year.

- Schedule D: This form is for reporting capital gains and losses from the sale of assets, such as stocks or real estate. It helps determine tax owed on these transactions.

- Form 8862: This form is used to claim the Earned Income Tax Credit (EITC) after previous disallowance. Taxpayers must provide information to prove eligibility for the credit.

- Form 8889: This form is required for reporting Health Savings Account (HSA) contributions and distributions. It helps taxpayers understand their tax benefits related to HSAs.

- Form 1040-SR: Designed for seniors, this form is similar to the 1040 but includes larger print and simplified language. It allows older taxpayers to file their returns easily.

Understanding these additional forms and documents can streamline the tax filing process. By gathering all necessary paperwork, taxpayers can ensure they meet their obligations and potentially maximize their refunds.

More PDF Forms

2b Mindset Tracker App - Log changes in your mood after meals for awareness.

A California Durable Power of Attorney form is a legal document that allows an individual to appoint someone else to make financial and legal decisions on their behalf, even if they become incapacitated. This form ensures that your wishes are respected and that your affairs are managed according to your preferences. For more information on how to create this important document, visit California Templates.

Waivers of Lien - The waiver is significant for ensuring compliance with local construction laws and regulations in Illinois.

Odometer Disclosure Statement Indiana - Standardized format recognized across many states for reliability.

Frequently Asked Questions

What is the IRS 1040 form?

The IRS 1040 form is the standard individual income tax return form used by U.S. taxpayers to report their annual income. It allows individuals to calculate their tax liability, claim tax credits, and determine if they owe additional taxes or are due a refund. The form consists of various sections where taxpayers report income, adjustments, deductions, and credits.

Who needs to file the IRS 1040 form?

Most U.S. citizens and residents who earn income are required to file the IRS 1040 form. This includes individuals who:

- Have a gross income that meets the filing threshold for their filing status.

- Are self-employed and earn a net profit.

- Receive income from sources such as rental properties, dividends, or interest.

- Wish to claim tax credits or refunds for withheld taxes.

Exceptions may apply for certain low-income individuals or those who qualify for specific tax benefits.

What are the main sections of the IRS 1040 form?

The IRS 1040 form is divided into several key sections, including:

- Personal Information: This section requires basic details such as name, address, and Social Security number.

- Income: Taxpayers report various types of income, including wages, salaries, and investment earnings.

- Deductions: Taxpayers can choose to take the standard deduction or itemize deductions to reduce taxable income.

- Tax and Credits: This section calculates the total tax owed and allows for the application of any tax credits.

- Payments: Taxpayers report any tax payments made throughout the year, including withholding and estimated payments.

- Refund or Amount Owed: The form concludes with a calculation of whether the taxpayer will receive a refund or owe additional taxes.

How can I file the IRS 1040 form?

Taxpayers have several options for filing the IRS 1040 form:

- Online: Many individuals choose to file electronically using tax preparation software or through the IRS e-file system.

- By Mail: Taxpayers can also complete a paper form and mail it to the appropriate IRS address. Forms can be downloaded from the IRS website or obtained at local libraries and post offices.

- Through a Tax Professional: Some individuals prefer to hire a tax professional to prepare and file their tax return.

Regardless of the method chosen, it is important to ensure that the form is filed by the tax deadline to avoid penalties.