Attorney-Approved Loan Agreement Form for Florida State

The Florida Loan Agreement form serves as a crucial document in the realm of lending, outlining the terms and conditions under which a borrower receives funds from a lender. This form typically includes essential details such as the loan amount, interest rate, repayment schedule, and any applicable fees. Both parties must agree on the duration of the loan, which can vary significantly depending on the nature of the agreement. Additionally, the form often stipulates the consequences of default, ensuring that both the lender and borrower are aware of their rights and obligations. It may also contain provisions for collateral, which serves as security for the loan, thereby protecting the lender's interests. By clearly delineating these aspects, the Florida Loan Agreement form aims to foster transparency and understanding between the parties involved, ultimately facilitating a smoother lending process.

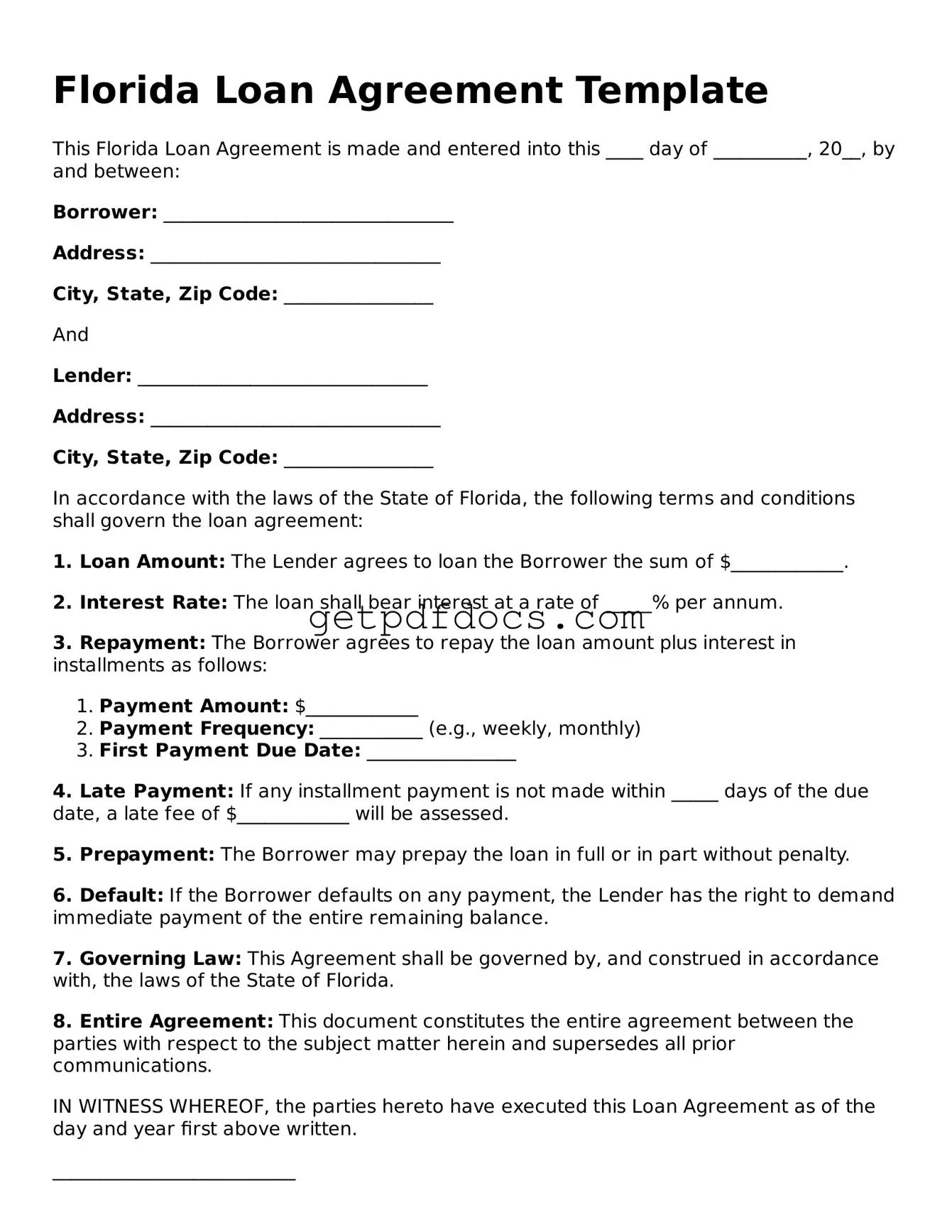

How to Use Florida Loan Agreement

Completing the Florida Loan Agreement form is an essential step in documenting the terms of a loan. By accurately filling out this form, both the lender and borrower can ensure clarity and mutual understanding of their obligations. Follow the steps below to fill out the form correctly.

- Obtain the form: Download the Florida Loan Agreement form from a reliable source or obtain a physical copy.

- Enter the date: Fill in the date when the agreement is being signed at the top of the form.

- Identify the parties: Clearly write the full names and addresses of both the lender and the borrower in the designated sections.

- Specify the loan amount: Indicate the total amount of money being loaned in the appropriate field.

- Detail the interest rate: Provide the agreed-upon interest rate, if applicable, in percentage form.

- Outline the repayment terms: Clearly describe the repayment schedule, including due dates and payment amounts.

- Include any fees: List any additional fees or charges associated with the loan, such as late fees or processing fees.

- Signatures: Ensure both the lender and borrower sign and date the form at the bottom to validate the agreement.

Key takeaways

When filling out and using the Florida Loan Agreement form, there are several important points to keep in mind. Understanding these key takeaways will help ensure that the process goes smoothly and that all parties are protected.

- Identify the Parties: Clearly state the names and contact information of both the lender and the borrower. This ensures that everyone knows who is involved in the agreement.

- Loan Amount: Specify the exact amount of money being loaned. This figure should be clear to avoid any confusion later on.

- Interest Rate: Include the interest rate applicable to the loan. Make sure to specify whether it is fixed or variable.

- Repayment Terms: Outline the repayment schedule. This should detail when payments are due and how they should be made.

- Late Fees: Clearly state any late fees that may apply if payments are not made on time. This can help encourage timely payments.

- Default Conditions: Define what constitutes a default on the loan. This helps both parties understand the consequences of failing to adhere to the agreement.

- Governing Law: Specify that the agreement will be governed by Florida law. This is crucial for resolving any potential disputes.

- Signatures: Ensure that both parties sign the agreement. This is a critical step in making the document legally binding.

- Witness or Notary: Consider having the agreement witnessed or notarized. This adds an extra layer of legitimacy to the document.

- Keep Copies: After the agreement is signed, both parties should keep copies for their records. This is important for reference in the future.

By following these key takeaways, individuals can navigate the Florida Loan Agreement form more effectively, ensuring clarity and legal protection for both parties involved.

Common mistakes

When filling out the Florida Loan Agreement form, many people make common mistakes that can lead to delays or complications. One frequent error is not providing complete information. Each section of the form requires specific details. Omitting even a small piece of information can cause processing issues.

Another mistake is using incorrect or outdated personal information. Borrowers should double-check their names, addresses, and contact details. Inaccurate information can lead to misunderstandings or disputes later on.

Many individuals also overlook the importance of reading the terms carefully. The Loan Agreement contains crucial details about interest rates, repayment schedules, and fees. Failing to understand these terms can result in unexpected costs or obligations.

Some people forget to sign the document. A signature is essential to validate the agreement. Without it, the document may not be considered legally binding, which can create problems for both the lender and the borrower.

Another common issue arises from not providing proper identification. Lenders typically require valid ID to verify the identity of the borrower. Failing to include this can delay the approval process.

Additionally, borrowers sometimes fail to keep copies of the completed form. Having a copy is important for personal records and can help resolve any future disputes or questions about the agreement.

Lastly, many individuals do not seek clarification when they encounter confusing sections. It’s perfectly acceptable to ask questions. Ignoring uncertainties can lead to mistakes that might have been easily avoided.

Documents used along the form

When entering into a loan agreement in Florida, several other forms and documents may be necessary to ensure that all parties are protected and that the terms of the loan are clearly understood. Here are four common documents that often accompany a Florida Loan Agreement:

- Promissory Note: This document outlines the borrower's promise to repay the loan amount under specified terms. It includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments.

- Articles of Incorporation: This form is essential for establishing a corporation in Florida and can be obtained through the Florida Forms website, ensuring all necessary details about the corporation are clearly outlined.

- Security Agreement: If the loan is secured by collateral, a security agreement is used to specify what assets are being pledged. This document protects the lender’s interests by providing a legal claim to the collateral if the borrower defaults on the loan.

- Loan Disclosure Statement: This statement provides important information about the loan terms, including the total cost of the loan, the annual percentage rate (APR), and any fees associated with the loan. It helps borrowers understand their financial obligations before signing the loan agreement.

- Personal Guarantee: In some cases, a lender may require a personal guarantee from the borrower or a third party. This document ensures that if the borrower defaults, the guarantor agrees to repay the loan, providing an additional layer of security for the lender.

Having these documents in place can help clarify the terms of the loan and protect the interests of both the lender and the borrower. It's essential to review each document carefully and ensure that all parties understand their rights and obligations before proceeding with the loan agreement.

Browse Other Common Loan Agreement Forms for Different States

Sample Promissory Note California - This form specifies the amount of the loan and the interest rate applied.

For those looking to ensure compliance with boat ownership transfer regulations, the California Templates offer a reliable option to access a fillable Boat Bill of Sale form that simplifies the process and helps avoid any potential legal ambiguities.

Frequently Asked Questions

What is a Florida Loan Agreement?

A Florida Loan Agreement is a legal document that outlines the terms and conditions under which a borrower receives funds from a lender. This agreement details the amount borrowed, interest rates, repayment schedule, and any collateral involved. It serves to protect both parties by clearly defining their rights and obligations.

Who can enter into a Florida Loan Agreement?

Any individual or business can enter into a Florida Loan Agreement, provided they are of legal age and have the capacity to contract. This includes personal loans between friends or family, as well as formal agreements with financial institutions or private lenders.

What are the key components of a Florida Loan Agreement?

A comprehensive Florida Loan Agreement typically includes the following components:

- Loan amount

- Interest rate

- Repayment terms

- Due dates for payments

- Consequences of default

- Any collateral securing the loan

- Signatures of both parties

Is it necessary to have a lawyer review the Loan Agreement?

While it is not legally required to have a lawyer review the Loan Agreement, it is highly advisable. A legal professional can ensure that the terms are fair and compliant with Florida laws, helping to prevent potential disputes in the future.

What happens if the borrower defaults on the loan?

If the borrower defaults on the loan, the lender may have several options available, depending on the terms outlined in the agreement. These may include:

- Charging late fees

- Initiating collection efforts

- Seizing collateral, if applicable

- Filing a lawsuit to recover the owed amount

Can a Loan Agreement be modified after it is signed?

Yes, a Loan Agreement can be modified after it is signed, but both parties must agree to the changes. It is essential to document any modifications in writing and have both parties sign the amended agreement to ensure clarity and enforceability.

What is the typical duration of a Loan Agreement?

The duration of a Loan Agreement can vary significantly depending on the terms negotiated between the borrower and lender. Agreements can range from short-term loans, lasting a few months, to long-term loans that may extend for several years.

Are there any state-specific regulations for Loan Agreements in Florida?

Yes, Florida has specific laws governing loan agreements, including interest rate limits and disclosure requirements. It is important for both parties to be aware of these regulations to ensure compliance and avoid potential legal issues.

What should I do if I have a dispute regarding the Loan Agreement?

If a dispute arises regarding the Loan Agreement, it is advisable to first attempt to resolve the issue directly with the other party. If this is unsuccessful, mediation or arbitration may be considered. Legal action can be a last resort if all other options fail.

How can I obtain a Florida Loan Agreement template?

A Florida Loan Agreement template can be obtained through various sources, including legal websites, local libraries, or by consulting with an attorney. It is crucial to ensure that any template used complies with Florida laws and is tailored to the specific needs of the parties involved.