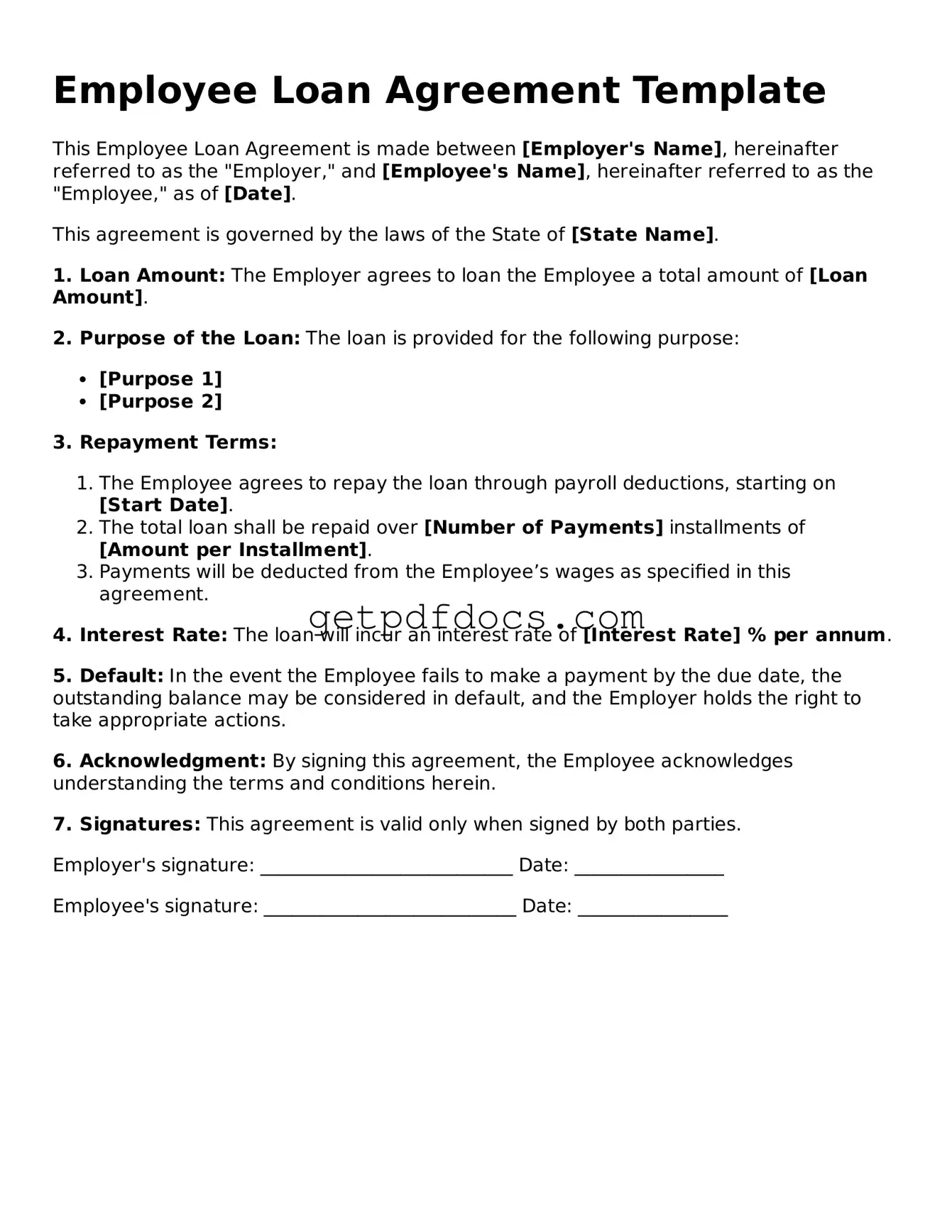

Printable Employee Loan Agreement Template

When navigating the complexities of employee financing, the Employee Loan Agreement form serves as a crucial tool for both employers and employees. This form outlines the specific terms and conditions under which a loan is provided, ensuring clarity and mutual understanding. Key elements typically included are the loan amount, repayment schedule, interest rate, and any applicable fees. Additionally, it addresses the consequences of default and the rights of both parties involved. By establishing these parameters, the agreement helps protect the interests of the employer while providing employees with the necessary financial support. A well-structured Employee Loan Agreement fosters transparency and trust, making it an essential document in the employer-employee relationship.

How to Use Employee Loan Agreement

Completing the Employee Loan Agreement form is a straightforward process that ensures both the employee and employer are on the same page regarding the loan's terms. Following these steps will help you fill out the form accurately and efficiently.

- Read the Form Carefully: Before starting, take a moment to read through the entire form. This will give you a clear understanding of what information is required.

- Provide Employee Information: Fill in your full name, employee ID, and contact information in the designated sections.

- Specify Loan Amount: Clearly indicate the amount of money being borrowed. Make sure this matches any verbal agreements made prior.

- Detail Loan Purpose: Briefly describe the reason for the loan. This helps clarify the intent behind the request.

- Set Repayment Terms: Outline the repayment schedule, including the amount and frequency of payments. Be specific about start dates and due dates.

- Include Interest Rate: If applicable, state the interest rate for the loan. Make sure this is agreed upon by both parties.

- Sign and Date: Both the employee and an authorized representative from the employer should sign and date the form at the bottom.

- Keep a Copy: After completing the form, make sure to keep a copy for your records. This will be important for future reference.

Key takeaways

Filling out and using the Employee Loan Agreement form requires attention to detail and a clear understanding of the terms involved. Here are some key takeaways to keep in mind:

- Accurate Information: Ensure that all personal and loan details are filled out accurately. This includes the employee's name, loan amount, repayment terms, and interest rates.

- Clear Terms: Clearly outline the repayment schedule. Specify the frequency of payments, due dates, and any penalties for late payments to avoid misunderstandings.

- Documentation: Keep a copy of the signed agreement for both the employer and employee. This serves as a reference point and can help resolve any disputes that may arise.

- Legal Compliance: Ensure that the agreement complies with relevant laws and company policies. This includes understanding any tax implications for both the employer and the employee.

By following these key points, both employers and employees can navigate the loan process more effectively and foster a transparent working relationship.

Common mistakes

When filling out the Employee Loan Agreement form, individuals often encounter several common pitfalls that can lead to confusion or delays. One frequent mistake is failing to provide accurate personal information. For example, missing or incorrect names, addresses, or contact details can complicate the processing of the loan. It is crucial to double-check all entries for accuracy to ensure smooth communication and record-keeping.

Another common error is neglecting to specify the loan amount clearly. This section should reflect the exact figure being requested. Rounding numbers or providing estimates can lead to misunderstandings. Clarity in this part of the form is essential for both the lender and the borrower to avoid any discrepancies later on.

Additionally, individuals sometimes overlook the importance of understanding the repayment terms. Failing to read and comprehend the terms can result in unexpected obligations. It is advisable to take the time to review the repayment schedule, interest rates, and any penalties for late payments. This understanding helps in planning for future payments and ensures that borrowers are fully aware of their commitments.

Another mistake involves not providing necessary documentation. The Employee Loan Agreement often requires supporting documents, such as proof of income or employment verification. Omitting these documents can delay the loan approval process. Always check the requirements and ensure that all necessary paperwork is attached before submission.

People may also forget to sign the form. A signature is often a critical component of the agreement, signifying acceptance of the terms outlined. Without a signature, the agreement may be considered incomplete, which can lead to further delays or complications in processing the loan.

Lastly, individuals sometimes fail to keep a copy of the completed form for their records. Retaining a copy can be beneficial for future reference, especially if questions arise about the loan terms or repayment. Keeping organized records helps in managing financial obligations more effectively.

Documents used along the form

When entering into an Employee Loan Agreement, several additional forms and documents may be required to ensure clarity and compliance. These documents serve various purposes, from outlining repayment terms to confirming the employee's understanding of the loan conditions. Below is a list of commonly used forms associated with the Employee Loan Agreement.

- Promissory Note: This document outlines the borrower's promise to repay the loan amount. It details the loan terms, including interest rates, repayment schedule, and consequences of default. It serves as a legal record of the loan agreement.

- Loan Application Form: This form collects essential information about the employee requesting the loan. It typically includes personal details, employment status, and the purpose of the loan. This information helps assess the employee's eligibility for the loan.

- Loan Agreement Form: For clear terms and responsibilities, refer to the comprehensive Loan Agreement documentation to ensure all parties are informed and protected.

- Repayment Schedule: A detailed plan that outlines when payments are due and the amount of each payment. This document helps both the employer and employee keep track of repayment timelines and ensures transparency throughout the loan period.

- Authorization for Payroll Deduction: This form allows the employer to automatically deduct loan payments from the employee's paycheck. It ensures that repayments are made consistently and on time, reducing the risk of missed payments.

- Loan Agreement Acknowledgment: This document confirms that the employee has read and understood the terms of the Employee Loan Agreement. It serves as a record that the employee is aware of their obligations and the consequences of failing to meet them.

These documents collectively help create a clear framework for the loan process, ensuring that both the employer and employee are on the same page. By utilizing these forms, the loan agreement can proceed smoothly, fostering trust and accountability between both parties.

Frequently Asked Questions

What is an Employee Loan Agreement?

An Employee Loan Agreement is a formal document that outlines the terms and conditions under which an employer provides a loan to an employee. This agreement typically includes details such as the loan amount, repayment schedule, interest rate (if applicable), and any other relevant terms. It serves to protect both the employer and the employee by clearly defining expectations and responsibilities.

Who is eligible to receive a loan under this agreement?

Eligibility for a loan under the Employee Loan Agreement can vary by organization. Generally, employees who have been with the company for a certain period and meet specific criteria, such as job performance and financial need, may qualify. It is essential to review the company's policy regarding employee loans to understand the specific requirements.

How is the repayment process structured?

The repayment process is typically outlined in the Employee Loan Agreement. Key components often include:

- Repayment schedule: This details when payments are due (e.g., bi-weekly, monthly).

- Loan term: This specifies the total duration over which the loan must be repaid.

- Interest rate: If applicable, the agreement will state the interest rate and how it is calculated.

Employees should ensure they understand these terms before signing the agreement, as they will be held accountable for adhering to the repayment schedule.

What happens if an employee cannot repay the loan?

If an employee is unable to repay the loan as agreed, it is crucial to communicate with the employer as soon as possible. Options may include renegotiating the repayment terms or setting up a temporary deferment. However, failure to repay the loan could lead to consequences such as deductions from future paychecks or negative impacts on the employee's credit rating.

Is the loan taxable income?

In many cases, loans provided to employees are not considered taxable income, provided they are structured correctly. However, if the loan is forgiven or if the terms are not followed, it may be treated as income and subject to taxation. Employees should consult with a tax professional to understand the implications of the loan on their tax situation.