Fill in a Valid Cg 20 10 07 04 Liability Endorsement Template

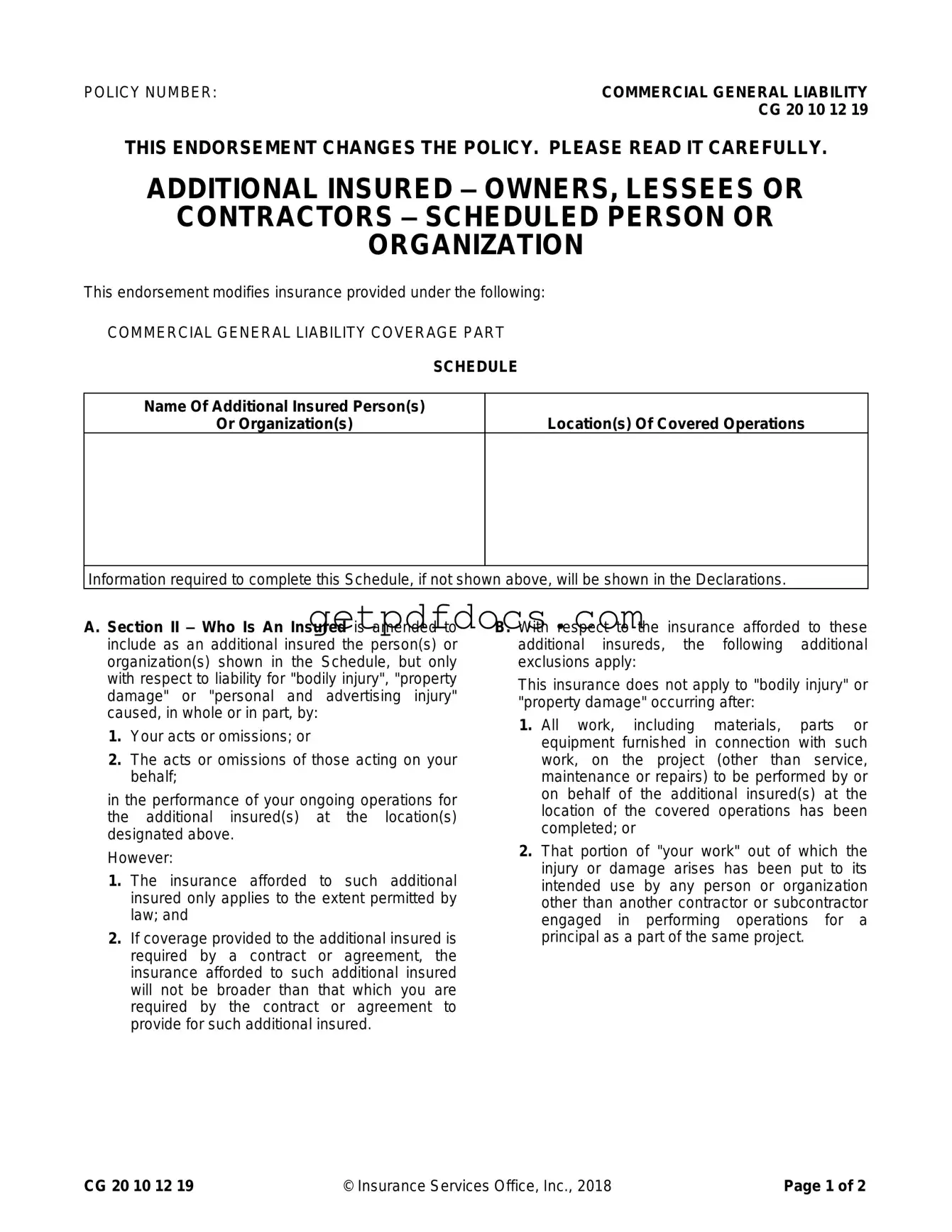

The CG 20 10 07 04 Liability Endorsement form is a critical document for businesses seeking to extend their insurance coverage to additional parties involved in their operations. This endorsement specifically modifies the Commercial General Liability policy, allowing for the inclusion of owners, lessees, or contractors as additional insureds. It outlines the necessary details, such as the names of the additional insured parties and the locations of covered operations. The endorsement ensures that these additional insureds are protected against liabilities arising from bodily injury, property damage, or personal and advertising injury caused by the actions of the primary insured or those acting on their behalf. However, it is important to note that the coverage is limited to the extent permitted by law and cannot exceed what is stipulated in any existing contracts. Furthermore, the endorsement includes specific exclusions, particularly concerning the timing of when the insurance applies, emphasizing that coverage ceases once the work is completed or the project is put to its intended use. Lastly, it establishes that the limits of insurance for the additional insureds will not exceed what is required by contract or the available policy limits, ensuring clarity in coverage expectations.

How to Use Cg 20 10 07 04 Liability Endorsement

Filling out the CG 20 10 07 04 Liability Endorsement form is a straightforward process that requires specific information to ensure accurate coverage for additional insured parties. Following the steps below will help ensure that the form is completed correctly.

- Locate the Policy Number section at the top of the form. Enter the relevant policy number associated with your Commercial General Liability coverage.

- In the Name of Additional Insured Person(s) or Organization(s) section, provide the full names of the individuals or organizations that need to be added as additional insureds. Ensure that spelling is accurate.

- Next, fill in the Location(s) of Covered Operations field. Specify the addresses or locations where the operations for the additional insureds will take place.

- Review the information entered for accuracy. Check that the names and locations are correct and complete.

- Sign and date the form in the designated area, confirming that the information provided is accurate and complete.

- Submit the completed form to your insurance provider or agent as instructed. Retain a copy for your records.

Key takeaways

Here are key takeaways regarding the CG 20 10 07 04 Liability Endorsement form:

- Purpose: This endorsement adds additional insured parties to a Commercial General Liability policy.

- Coverage Scope: It covers liability for bodily injury, property damage, and personal and advertising injury.

- Conditions: Coverage applies only if the injury or damage arises from the acts or omissions of the insured or those acting on their behalf.

- Contractual Limitations: If coverage is required by a contract, it cannot exceed what the contract stipulates.

- Completion of Work: Coverage does not apply after all work on the project has been completed.

- Intended Use Exclusion: If the work has been put to its intended use, coverage for related injuries or damages is excluded.

- Insurance Limits: The maximum payout for additional insureds is limited to the lesser of the contract requirements or the policy limits.

- Amendment to Insured Definition: Section II of the policy is amended to include the additional insureds listed in the schedule.

- Read Carefully: The endorsement modifies the original policy, necessitating careful review to understand its implications.

- Documentation: Ensure that all necessary information is filled out accurately in the schedule section of the form.

Common mistakes

Filling out the CG 20 10 07 04 Liability Endorsement form can be a straightforward process, but many individuals make common mistakes that can lead to complications down the line. One of the first mistakes is failing to include all required information in the "Schedule" section. This section is crucial because it specifies the names of additional insured parties and the locations of covered operations. Omitting any details here can result in coverage gaps, leaving you vulnerable in case of a claim.

Another frequent error involves misunderstanding the scope of coverage. Some people mistakenly believe that the endorsement automatically provides broad coverage to additional insureds without limitations. However, it’s essential to remember that the insurance only applies to liabilities arising from your acts or omissions or those of your representatives. Misinterpreting this can lead to unexpected liabilities that you thought were covered.

Additionally, individuals often overlook the importance of contract requirements. If the coverage for additional insureds is mandated by a contract, the insurance provided will not exceed what is specified in that contract. This misunderstanding can create a false sense of security, leading to potential disputes if a claim arises and the coverage is found to be insufficient.

Another mistake is neglecting to review the exclusions listed in the endorsement. Many people skip this section, assuming that all types of claims are covered. However, the endorsement specifically excludes coverage for "bodily injury" or "property damage" that occurs after the work has been completed or when the work has been put to its intended use. Failing to acknowledge these exclusions can result in significant financial repercussions.

Some individuals also make the error of not updating the form when changes occur. If new additional insureds need to be added or if there are changes to the locations of covered operations, it’s vital to update the endorsement promptly. Ignoring these updates can lead to confusion and disputes in the event of a claim.

Another common oversight is not keeping a copy of the completed form. Once the form is filled out, it’s important to retain a copy for your records. This documentation can be critical if any questions or issues arise regarding coverage in the future. Without a copy, you may find it difficult to prove what was agreed upon.

Finally, many people fail to seek clarification when they encounter confusing terms or sections within the form. If something is unclear, it’s always best to ask for help. Whether it’s from an insurance agent or a legal professional, getting clarification can prevent costly mistakes and ensure that the endorsement is filled out correctly.

Documents used along the form

The CG 20 10 07 04 Liability Endorsement form is a crucial document that helps clarify the coverage provided to additional insured parties in a commercial general liability insurance policy. However, it often works in conjunction with other important forms and documents. Understanding these related documents can help ensure that all parties are adequately protected and informed about their insurance coverage.

- Certificate of Insurance (COI): This document serves as proof of insurance coverage. It outlines the types of insurance a business holds, including policy numbers, coverage limits, and the effective dates of the policies. A COI is often requested by clients or contractors to verify that the necessary insurance is in place before work begins.

- Additional Insured Endorsement: This endorsement expands coverage to include additional parties, such as subcontractors or property owners, under the primary policy. It specifies the rights and responsibilities of these additional insureds, ensuring they receive protection against claims related to the insured's operations.

- Dirt Bike Bill of Sale: To facilitate the transfer of ownership for dirt bikes, completing the California Templates is essential for ensuring a smooth transaction.

- Contractual Liability Endorsement: This document modifies the liability coverage to include obligations assumed in contracts. It ensures that the insurer covers liabilities that arise from contracts, which may not be included in standard policies. This is particularly important for businesses that frequently enter into agreements with clients or other contractors.

- Waiver of Subrogation: This form prevents the insurance company from seeking reimbursement from a third party for claims paid. By signing this document, the insured agrees not to hold the additional insured responsible for damages, which can foster better relationships and reduce disputes between parties involved in a project.

By familiarizing yourself with these related documents, you can better navigate the complexities of insurance coverage. Each form plays a distinct role in protecting the interests of all parties involved, ensuring that everyone has the necessary coverage in place to handle potential liabilities effectively.

More PDF Forms

Florida Immunization Registry - The form addresses both specific vaccine doses and overall immunization status.

Creating a Last Will and Testament is essential for anyone looking to ensure their wishes are honored after they pass away. The Florida Last Will and Testament form is a legal document that allows individuals to specify how their property and affairs should be managed and distributed after their death. It serves as a critical tool for estate planning, ensuring that one's wishes are respected and loved ones are taken care of according to their desires. By detailing the distribution of assets, guardianship of minor children, and the selection of an executor, it provides peace of mind and clarity for all involved. For more information, you can refer to the form at https://floridaforms.net/blank-last-will-and-testament-form.

How to Write Payroll Checks - A document representing the financial transaction of employee pay.

Childcare Receipt Template - Appropriate document management practices enhance the credibility of child care providers.

Frequently Asked Questions

What is the purpose of the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form is designed to add additional insured parties to a commercial general liability insurance policy. This means that certain individuals or organizations can be covered under your policy for specific liabilities that arise from your actions or the actions of those working on your behalf. It is important for ensuring that all parties involved in a project are protected against potential claims of bodily injury, property damage, or personal and advertising injury.

Who qualifies as an additional insured under this endorsement?

The endorsement allows for the inclusion of specific individuals or organizations as additional insureds, provided their names are listed in the schedule section of the endorsement. This coverage applies only in relation to liabilities arising from your ongoing operations for those additional insureds at the designated locations. It is essential that the additional insureds are clearly identified to ensure proper coverage.

What types of liabilities are covered?

The endorsement covers liabilities related to bodily injury, property damage, and personal and advertising injury. However, this coverage is only applicable if the injury or damage was caused, in whole or in part, by your actions or the actions of those acting on your behalf during the performance of work for the additional insureds at the specified locations.

Are there any limitations to the coverage provided?

Yes, there are limitations. The coverage for additional insureds is only effective to the extent permitted by law. Additionally, if a contract or agreement requires coverage for the additional insured, the insurance provided cannot be broader than what is stipulated in that contract. Furthermore, coverage does not apply if the bodily injury or property damage occurs after all work on the project has been completed or after the work has been put to its intended use by someone other than another contractor or subcontractor involved in the project.

How does the endorsement affect the limits of insurance?

The endorsement does not increase the overall limits of your insurance policy. If coverage for the additional insured is required by a contract, the maximum amount payable on behalf of the additional insured will be the lesser of the amount specified in the contract or the applicable limits of your insurance policy. This ensures that the coverage remains consistent with the terms of the original policy.

What information is needed to complete the endorsement?

To complete the endorsement, you will need to provide the names of the additional insured individuals or organizations and the locations where the covered operations will take place. This information is typically included in the schedule section of the endorsement. If this information is not provided upfront, it will be specified in the policy declarations.

Can the coverage be modified after the endorsement is issued?

Once the endorsement is issued, any modifications to the coverage or the parties listed as additional insureds will typically require a new endorsement or an amendment to the existing policy. It is crucial to communicate any changes in operations or relationships with additional insureds to ensure that coverage remains valid and effective.

Is there a specific duration for the coverage provided?

The coverage under this endorsement is generally tied to the duration of the ongoing operations for the additional insureds at the specified locations. Once the work is completed or the project is put to its intended use, the coverage for that particular additional insured will cease. It is important to monitor the status of the project to understand when coverage may no longer apply.