Attorney-Approved Deed in Lieu of Foreclosure Form for California State

In California, homeowners facing financial difficulties may find the Deed in Lieu of Foreclosure to be a viable alternative to the lengthy and often stressful foreclosure process. This legal document allows a homeowner to voluntarily transfer ownership of their property to the lender in exchange for the cancellation of the mortgage debt. By choosing this route, individuals can avoid the negative consequences associated with foreclosure, such as a significant drop in credit score and the potential for legal complications. The Deed in Lieu of Foreclosure form must be completed accurately and submitted to the lender, who will then review the homeowner’s financial situation and property condition. This form typically includes essential details such as the property description, the names of the parties involved, and any existing liens or encumbrances. It is crucial for homeowners to understand that while this option can provide a fresh start, it may still have implications for their credit and future borrowing capabilities. Therefore, thorough consideration and consultation with a financial advisor or legal expert are recommended before proceeding with this option.

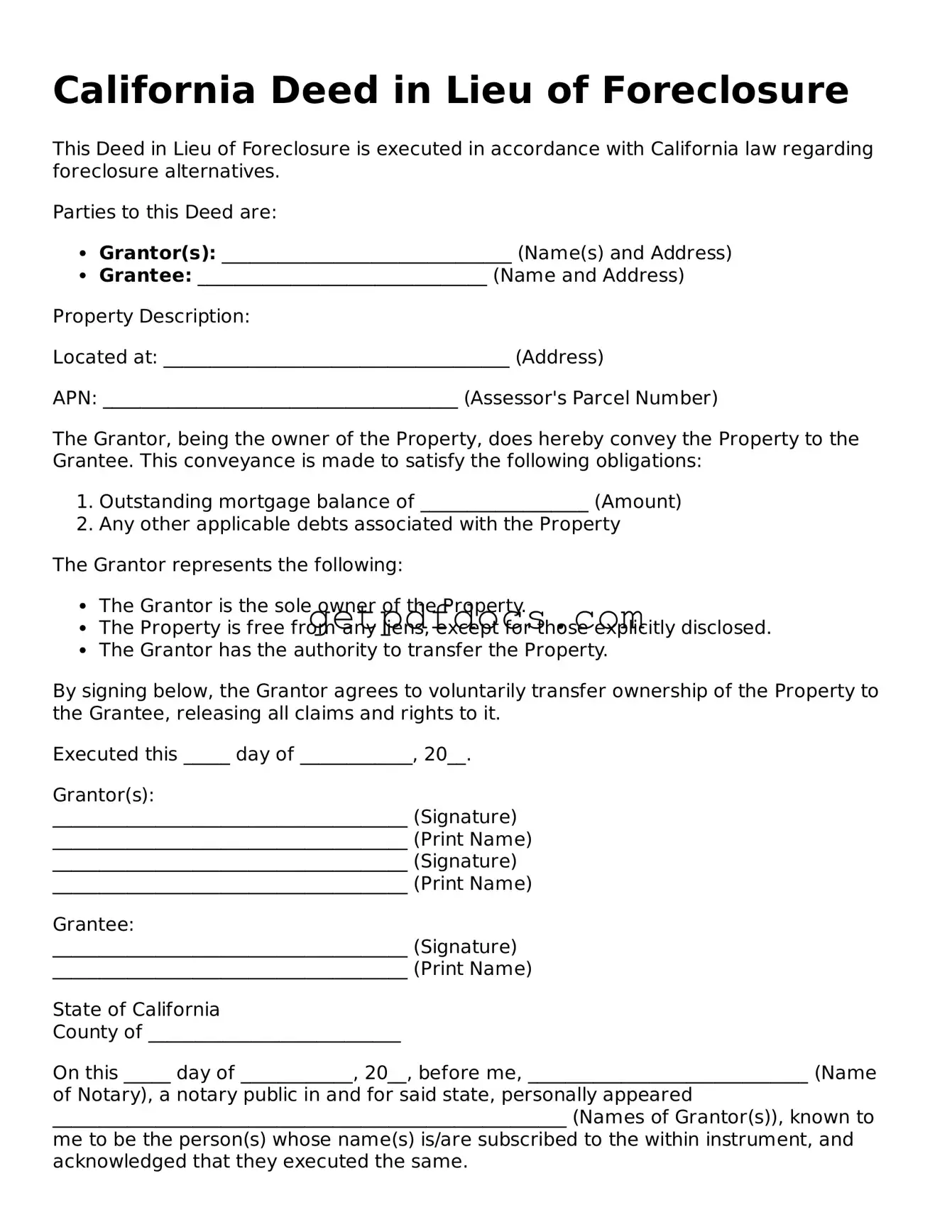

How to Use California Deed in Lieu of Foreclosure

Once you have decided to proceed with a Deed in Lieu of Foreclosure, it is essential to complete the necessary form accurately. This document transfers ownership of your property back to the lender, and it is crucial to ensure that all information is filled out correctly to avoid any delays in the process.

- Begin by obtaining the California Deed in Lieu of Foreclosure form. This can typically be found on your lender's website or through legal resources.

- At the top of the form, enter the date on which you are completing the document.

- Provide your name and address in the designated sections. Ensure that your name matches the name on the property title.

- Next, include the lender's name and address. Verify that you have the correct contact information for your lender.

- Fill in the property description. This should include the address and any legal description required. Refer to your property deed if necessary.

- Indicate whether there are any existing liens or encumbrances on the property. Be honest and thorough, as this information is crucial for the lender.

- Sign the form in the designated area. Your signature should match the name listed on the property title.

- Have the form notarized. This step is important for the document to be legally binding.

- Make copies of the completed form for your records before sending it to the lender.

- Submit the signed and notarized form to your lender. Ensure that you keep a record of the submission date and method of delivery.

After submitting the form, it is advisable to follow up with your lender to confirm receipt and to inquire about the next steps in the process. Maintaining open communication can help ensure a smooth transition.

Key takeaways

Filling out and utilizing the California Deed in Lieu of Foreclosure form can be a significant step for homeowners facing financial difficulties. Here are some key takeaways to consider:

- Understanding the Purpose: This form allows a homeowner to transfer their property back to the lender, thereby avoiding the lengthy and often costly foreclosure process.

- Eligibility Requirements: Not all homeowners qualify. Generally, the borrower must be facing financial hardship and must have a valid reason for choosing this option over foreclosure.

- Impact on Credit: While a deed in lieu of foreclosure is less damaging than a foreclosure, it can still negatively affect your credit score. It is crucial to understand the long-term implications.

- Negotiation with Lenders: Homeowners should communicate with their lenders before submitting the form. Some lenders may offer alternatives or negotiate terms that can be more favorable.

- Legal Considerations: Although the process may seem straightforward, it is advisable to consult with a legal professional to ensure that all aspects are handled correctly and that your rights are protected.

By keeping these points in mind, homeowners can navigate the process more effectively and make informed decisions regarding their property and financial future.

Common mistakes

Filling out a California Deed in Lieu of Foreclosure form can be a daunting task, and many people make common mistakes that can complicate the process. One frequent error is failing to include all necessary parties. It’s crucial to ensure that all individuals listed on the title are included in the deed. Omitting a co-owner can lead to legal complications later on.

Another mistake often made is not providing accurate property descriptions. The form requires a detailed description of the property, including the address and legal description. Inaccuracies can delay the process or even invalidate the deed.

People sometimes overlook the importance of signatures. Each party involved must sign the document. If even one signature is missing, the deed may not be considered valid. Additionally, forgetting to have the signatures notarized can also lead to issues, as notarization is often required for the deed to be legally binding.

Failing to understand the implications of the deed is another common error. A deed in lieu of foreclosure can affect your credit score and future borrowing ability. Many people fill out the form without fully grasping these consequences, which can lead to regret later.

Another mistake is neglecting to communicate with the lender. Before submitting the deed, it's important to discuss the process with the lender. Some lenders may have specific requirements or forms that need to be completed in conjunction with the deed.

People often rush through the process, leading to errors. Taking the time to review the form carefully can prevent mistakes. A hasty approach may result in overlooked details that could complicate the transaction.

Some individuals fail to keep copies of the completed form and any related documents. Having a record is essential for future reference. If questions arise later, having these documents can provide clarity and support your case.

Another common error is misunderstanding the tax implications. A deed in lieu of foreclosure can have tax consequences, such as potential liability for cancellation of debt income. Consulting a tax professional before submitting the deed is advisable.

Finally, people sometimes ignore deadlines. There may be specific timelines for submitting the deed to the lender. Missing these deadlines can result in a lost opportunity to avoid foreclosure.

By being aware of these common mistakes, individuals can navigate the process more smoothly and ensure that their Deed in Lieu of Foreclosure is completed correctly.

Documents used along the form

When dealing with a Deed in Lieu of Foreclosure in California, several other forms and documents may be necessary to ensure a smooth process. Understanding these documents can help homeowners and lenders navigate the complexities of property transfer and foreclosure alternatives. Here’s a brief overview of some key forms you might encounter.

- Notice of Default: This document is filed by the lender to inform the borrower that they are in default on their mortgage payments. It serves as an official warning before foreclosure proceedings begin.

- Loan Modification Agreement: This agreement outlines changes to the original loan terms, which may include a lower interest rate or extended repayment period. It aims to make the mortgage more manageable for the borrower.

- Short Sale Agreement: In cases where the property is sold for less than the amount owed on the mortgage, this document outlines the terms of the sale and requires lender approval. It allows the borrower to avoid foreclosure while selling the property.

- Release of Liability: This document releases the borrower from further obligations on the loan after the property is transferred. It is crucial for ensuring that the borrower is not held responsible for any remaining debt after the deed transfer.

- Property Inspection Report: Before the transfer of the deed, a property inspection may be conducted. This report assesses the condition of the property and identifies any issues that may need addressing prior to the deed in lieu process.

- Last Will and Testament Form: For those looking to secure their final wishes, the important Last Will and Testament document outlines how assets are handled after death.

- Settlement Statement: This document outlines the financial details of the transaction, including any fees, credits, and the final amount exchanged. It provides transparency for both parties involved in the deed transfer.

- Affidavit of Title: This sworn statement confirms that the seller has clear title to the property and has the right to transfer ownership. It protects the buyer from any future claims against the property.

Having a clear understanding of these documents can significantly ease the process of a Deed in Lieu of Foreclosure. Each form plays a vital role in ensuring that both the borrower and lender are protected throughout the transaction. Always consider consulting a professional if you have questions about specific documents or the overall process.

Browse Other Common Deed in Lieu of Foreclosure Forms for Different States

Sample Deed in Lieu of Foreclosure - The process may allow for a smoother transition to rental agreements or alternative housing solutions.

When engaging in the sale or purchase of an RV in Arizona, it is crucial to utilize the proper documentation, such as the Arizona PDFs, to ensure that all transactional details are recorded accurately and legally, thereby protecting both the buyer and seller throughout the process.

Frequently Asked Questions

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to voluntarily transfer the title of their property to the lender in order to avoid the foreclosure process. This option can be beneficial for both the homeowner and the lender, as it can save time and costs associated with foreclosure proceedings.

Who is eligible for a Deed in Lieu of Foreclosure?

Eligibility for a Deed in Lieu of Foreclosure typically depends on the lender's policies and the homeowner's financial situation. Generally, homeowners facing financial hardship, such as job loss or medical emergencies, may qualify. However, the property must also be free of other liens, or the lender must agree to accept the property with those liens.

What are the benefits of a Deed in Lieu of Foreclosure?

There are several advantages to choosing a Deed in Lieu of Foreclosure:

- It can help the homeowner avoid the lengthy and often stressful foreclosure process.

- The homeowner may be able to negotiate a more favorable outcome, such as a waiver of deficiency judgments.

- It allows the homeowner to leave the property without the stigma of foreclosure on their credit report.

- Lenders can save money and time by avoiding the foreclosure process.

What are the potential downsides?

While there are benefits, there are also potential downsides to consider:

- The homeowner may still face tax implications on any forgiven debt.

- Not all lenders accept Deeds in Lieu of Foreclosure, which may limit options.

- It may not be suitable for homeowners who wish to keep their property.

How does the process work?

The process typically involves several steps:

- The homeowner contacts their lender to discuss the possibility of a Deed in Lieu of Foreclosure.

- The lender reviews the homeowner's financial situation and the property's status.

- If approved, the homeowner and lender will draft the Deed in Lieu of Foreclosure document.

- Once signed, the homeowner transfers the title to the lender.

- The lender may then release the homeowner from further obligations related to the mortgage.

Will I still owe money after signing a Deed in Lieu of Foreclosure?

In many cases, homeowners can negotiate with their lender to waive any remaining debt after the property is transferred. However, this is not guaranteed. It is essential to clarify this point with the lender before proceeding.

Can I still apply for a Deed in Lieu of Foreclosure if I am already in foreclosure?

Yes, it is possible to apply for a Deed in Lieu of Foreclosure even if you are already facing foreclosure. However, the lender may require you to demonstrate that you have made efforts to resolve the situation before considering this option.

What documentation is needed for a Deed in Lieu of Foreclosure?

Homeowners will typically need to provide various documents, including:

- Proof of income and financial hardship.

- Details about the property, such as its current value and condition.

- Any relevant loan documents.

Is legal assistance recommended?

While it is not required, seeking legal assistance can be beneficial. A legal professional can help navigate the process, ensure that the homeowner's rights are protected, and negotiate terms with the lender effectively.

How does a Deed in Lieu of Foreclosure affect my credit score?

A Deed in Lieu of Foreclosure will likely have a negative impact on your credit score, but it may be less severe than a full foreclosure. The exact effect can vary based on individual circumstances and the specific scoring model used by lenders.