Fill in a Valid Business Credit Application Template

The Business Credit Application form serves as a vital tool for businesses seeking to establish credit relationships with suppliers and lenders. This document collects essential information about the applicant's business, including its legal structure, ownership details, and financial history. Key components often include the business's name, address, and contact information, as well as the names of the owners or principals. Financial information, such as annual revenue, bank references, and trade references, is typically required to assess the creditworthiness of the applicant. Additionally, the form may request details regarding the business's credit needs and the intended use of the credit. By providing this information, businesses can facilitate a smoother credit approval process, allowing suppliers and lenders to make informed decisions. Understanding the significance of each section of the form can help ensure that all necessary information is accurately presented, ultimately contributing to a successful application outcome.

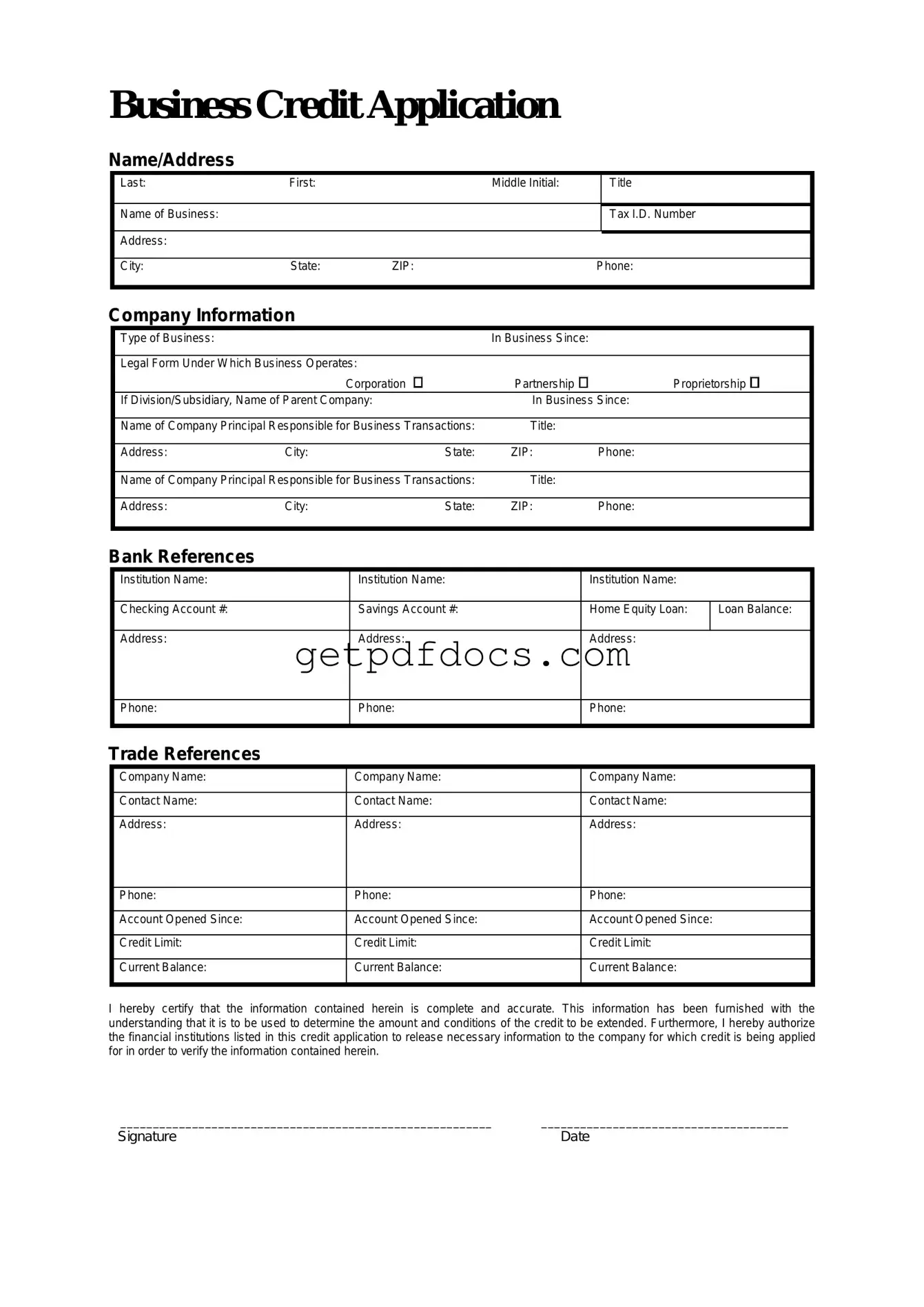

How to Use Business Credit Application

Once you have the Business Credit Application form in hand, you'll need to complete it accurately to ensure a smooth processing experience. The following steps will guide you through filling out the form correctly.

- Begin by entering your business name at the top of the form.

- Provide your business address, including street, city, state, and zip code.

- List your business phone number and email address for contact purposes.

- Indicate the type of business (e.g., sole proprietorship, partnership, corporation).

- Fill in the federal tax ID number or your social security number if applicable.

- Provide the names of the owners or principal officers of the business.

- Include the length of time the business has been operating.

- Detail your banking information, including the name of your bank and account numbers.

- List any trade references, including company names and contact information.

- Finally, sign and date the form to certify that all information is accurate.

Key takeaways

Filling out and using the Business Credit Application form is a crucial step for any business seeking credit. Here are some key takeaways to ensure the process goes smoothly:

- Accuracy is Essential: Ensure that all information provided is accurate and up-to-date. Mistakes can lead to delays or denial of credit.

- Provide Complete Information: Fill out all sections of the application. Incomplete forms may be rejected or require additional follow-up.

- Know Your Business: Be prepared to provide details about your business structure, including ownership, years in operation, and industry type.

- Financial Information Matters: Include relevant financial statements, such as balance sheets and income statements, to support your application.

- Credit History: Be ready to disclose your business's credit history. This includes previous loans, payment history, and any outstanding debts.

- References: Provide references from suppliers or other creditors who can vouch for your business's creditworthiness.

- Review Before Submission: Double-check your application for errors or omissions before submitting it to avoid processing delays.

- Follow Up: After submission, follow up with the lender to confirm receipt and inquire about the timeline for a decision.

- Understand Terms: Familiarize yourself with the terms of credit being offered, including interest rates, repayment terms, and fees.

By keeping these points in mind, businesses can enhance their chances of successfully obtaining credit and establishing a solid financial foundation.

Common mistakes

Filling out a Business Credit Application form can seem straightforward, but many people trip up along the way. One common mistake is providing incomplete information. Omitting essential details like your business address or contact information can lead to delays or even denial of credit. Always double-check that every section is filled out completely before submitting.

Another frequent error is using outdated financial information. Financial stability is a key factor in creditworthiness. If your application reflects old data, it may not accurately represent your current situation. Keep your financial statements up to date and ensure they reflect your business's current health.

Some applicants fail to understand the importance of accuracy. Typos and inaccuracies can create a negative impression. A simple misspelling of your business name or incorrect figures can raise red flags for lenders. Take the time to proofread your application to avoid these pitfalls.

Many people also underestimate the significance of their business credit history. If you have a poor credit history, it’s crucial to be upfront about it. Hiding negative information can backfire. Instead, be honest and explain any past issues, along with how you’ve improved since then.

Another mistake is neglecting to include relevant supporting documents. Lenders often require additional paperwork, such as tax returns or financial statements, to assess your application accurately. Failing to provide these documents can lead to unnecessary delays or a rejection of your application.

Some applicants forget to review the terms and conditions of the credit being offered. Understanding the interest rates, repayment terms, and any fees associated with the credit is essential. Failing to do so can lead to unexpected financial burdens down the line.

Additionally, many people overlook the importance of a personal guarantee. If your business is new or lacks a strong credit history, lenders may require a personal guarantee. Not mentioning this upfront can complicate the approval process later.

Finally, rushing through the application can lead to errors. It’s easy to think that a quick submission is better, but taking your time ensures accuracy and completeness. Set aside dedicated time to fill out the application thoughtfully.

Documents used along the form

When applying for business credit, several forms and documents complement the Business Credit Application. Each plays a critical role in providing a comprehensive view of your business's financial health and stability. Here are some essential documents to consider:

- Personal Guarantee: This document outlines that the business owner agrees to be personally responsible for the debt incurred by the business. Lenders often require this to mitigate their risk.

- Business Financial Statements: Typically including balance sheets and income statements, these documents give lenders insight into the financial performance and health of your business over a specified period.

- Residential Lease Agreement Form: For clear rental terms, utilize the comprehensive Residential Lease Agreement template to outline the responsibilities of landlords and tenants in Florida.

- Tax Returns: Providing personal and business tax returns for the past few years can help demonstrate your financial stability and history. Lenders often look for consistency and growth in these records.

- Business Plan: A well-structured business plan outlines your business goals, strategies, and financial projections. This helps lenders understand your vision and how you plan to achieve it.

- Credit Report: A credit report details your business's credit history and can influence a lender's decision. It's wise to review this report beforehand to ensure accuracy.

- Legal Documents: Depending on your business structure, you may need to provide documents like articles of incorporation, partnership agreements, or operating agreements. These establish the legitimacy of your business entity.

Gathering these documents can streamline the credit application process and improve your chances of securing the financing you need. Each piece of information contributes to a clearer picture of your business's viability and reliability as a borrower.

More PDF Forms

Tax Form Schedule C - It establishes a narrative for financial performance that can enhance stakeholder trust.

The California Employment Verification form is a crucial document used to confirm an individual's employment status and details. This form is often required for various purposes, such as loan applications or rental agreements. For further assistance in filling out this essential form, you can refer to the available resources at California Templates. Understanding how to fill it out correctly can streamline your verification process, so be sure to complete the form by clicking the button below.

Fedx Freight - Delivery options include priority, A.M. delivery, and economy service.

Alabama Public Title Portal - The lien date for transferred liens should remain unchanged during this process.

Frequently Asked Questions

What is a Business Credit Application form?

The Business Credit Application form is a document that businesses fill out to request credit from a lender or supplier. This form collects essential information about your business, including its financial status, credit history, and ownership details. Completing this form accurately is crucial for obtaining credit terms that suit your business needs.

What information do I need to provide on the form?

When filling out the Business Credit Application form, you will typically need to provide the following information:

- Business Information: This includes your business name, address, and contact details.

- Ownership Details: Names and addresses of the business owners or partners.

- Financial Information: Your business's annual revenue, bank references, and any outstanding debts.

- Credit History: Information about your previous credit accounts and payment history.

Make sure to review all sections carefully to ensure accuracy and completeness.

How long does it take to process the application?

The processing time for a Business Credit Application can vary based on the lender or supplier. Generally, you can expect a response within a few business days. However, if additional information is needed, it may take longer. It's always a good idea to follow up if you haven't received a response within the expected timeframe.

What happens if my application is denied?

If your application is denied, you will typically receive a notification explaining the reasons for the denial. Common reasons include insufficient credit history, low revenue, or high existing debt. If you believe there was an error or if your situation has changed, you can consider reapplying or contacting the lender for further clarification.

Can I appeal a denied application?

Yes, you can appeal a denied Business Credit Application. Start by reviewing the reasons for the denial, then gather any additional documentation that may support your case. Reach out to the lender or supplier to discuss your situation. They may allow you to provide new information or clarify any misunderstandings that led to the denial.