Fill in a Valid Acord 130 Template

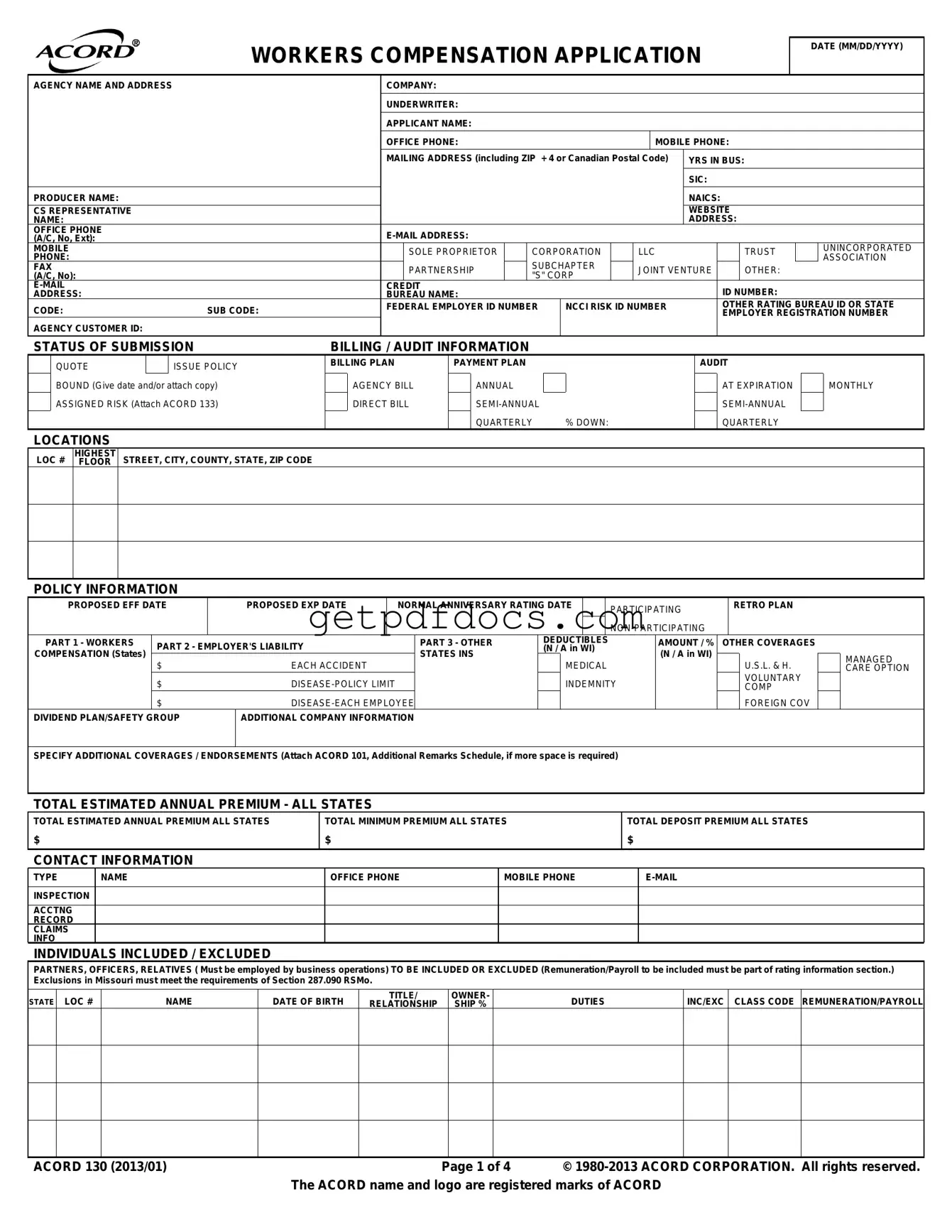

The Acord 130 form serves as a crucial document in the workers' compensation insurance application process. It collects essential information about the applicant's business, including the agency name, contact details, and business structure, such as whether the entity is a corporation, partnership, or sole proprietorship. The form requires applicants to disclose their years in business, industry classifications, and relevant identification numbers, which assist insurers in assessing risk. Additionally, it includes sections for policy information, proposed effective dates, and estimated annual premiums. The Acord 130 also addresses the specifics of coverage, including workers' compensation, employer's liability, and any additional endorsements that may be necessary. Furthermore, the form captures loss history and prior carrier information, providing insurers with a comprehensive view of the applicant's risk profile. By requiring detailed information about employees, operations, and safety practices, the Acord 130 facilitates informed underwriting decisions and helps ensure that businesses receive appropriate coverage tailored to their needs.

How to Use Acord 130

Filling out the ACORD 130 form is an important step in applying for workers' compensation insurance. It requires specific information about your business and its operations. Make sure to have all necessary details at hand to ensure a smooth completion of the form.

- Enter the Application Date: Fill in the date at the top of the form in MM/DD/YYYY format.

- Agency Information: Provide your agency name and address.

- Company and Underwriter: Fill in the names of the insurance company and underwriter.

- Applicant Information: Enter your name, office phone, and mobile phone.

- Mailing Address: Include your complete mailing address, including ZIP + 4 or Canadian Postal Code.

- Business Details: Indicate the years in business and your SIC (Standard Industrial Classification) and NAICS (North American Industry Classification System) codes.

- Producer and CS Representative: Fill in the producer's name, website, and contact details.

- Business Structure: Select the appropriate business structure (e.g., sole proprietor, corporation, LLC, etc.).

- Federal Employer ID Number: Provide your Federal Employer ID Number and NCCI Risk ID Number if applicable.

- Policy Information: Enter the proposed effective and expiration dates of the policy, along with the normal anniversary rating date.

- Coverage Information: Fill in the details for workers' compensation, employer's liability, and any other coverages needed.

- Estimated Annual Premium: Provide the total estimated annual premium for all states.

- Contact Information: Include the contact details for individuals involved in inspection, accounting, and claims.

- Employee Information: List any individuals included or excluded from coverage, along with their details.

- Rating Information: Fill in the state rating worksheet for multiple states if applicable.

- Prior Carrier Information: Provide information on your past five years of insurance coverage and loss history.

- General Information: Answer all yes/no questions and provide explanations where necessary.

- Signature: Ensure that the applicant's signature is provided, along with the date and producer's signature.

After completing the form, review all entries for accuracy. It’s essential to ensure that all information is correct before submitting the application to avoid delays in processing. Keep a copy for your records as well.

Key takeaways

- Complete All Sections: Ensure that every section of the Acord 130 form is filled out accurately. Missing information can delay processing and lead to issues with coverage.

- Provide Accurate Premium Estimates: Carefully estimate your total annual premium and minimum premium. This information is crucial for determining your policy costs.

- Include All Employees: List all employees, including partners and relatives, who are part of the business operations. This helps in assessing risk and determining coverage needs.

- Be Honest About Operations: Answer all questions truthfully, especially regarding past claims and any hazardous materials. Misleading information can lead to penalties or denial of claims.

Common mistakes

Filling out the ACORD 130 form is a crucial step in obtaining workers' compensation insurance. However, many applicants make mistakes that can lead to delays or even denials of coverage. Understanding these common errors is essential for ensuring a smooth application process.

One frequent mistake is incomplete contact information. Applicants often forget to provide accurate phone numbers or email addresses. This can hinder communication between the insurer and the applicant, leading to missed opportunities for clarification or additional information. Always double-check that all contact details are correct and up-to-date.

Another common error involves misreporting the number of employees. It is vital to accurately represent the number of full-time and part-time employees. Misunderstanding or miscalculating this information can affect the premium and coverage options. Insurers rely on these figures to assess risk, so providing precise numbers is critical.

Many applicants also overlook the importance of detailing business operations. The form requires a clear description of the nature of the business and its operations. Vague or incomplete descriptions can lead to misunderstandings about the risks associated with the business. Take the time to provide thorough and specific information to avoid complications later on.

Additionally, failing to disclose prior claims history is a significant mistake. Insurers need to know about any past claims to assess risk accurately. Omitting this information can raise red flags and potentially lead to coverage being denied. Be honest and forthcoming about any previous claims.

Another area where applicants stumble is in the classification of employees. The form requires specific classifications for different roles within the company. Misclassifying employees can result in incorrect premium calculations and could lead to penalties. Ensure that each employee's role is accurately classified according to the insurer's guidelines.

Lastly, applicants often neglect to review the form for errors before submission. Simple typos or inaccuracies can have serious consequences. A thorough review of the entire application can catch mistakes that could delay the approval process. It is wise to have a second pair of eyes look over the application to ensure everything is correct.

In conclusion, taking the time to avoid these common mistakes can greatly enhance the chances of a successful application for workers' compensation insurance. Each detail matters, and diligence in completing the ACORD 130 form can save time, money, and frustration in the long run.

Documents used along the form

The Acord 130 form is essential for applying for workers' compensation insurance. However, several other forms and documents often accompany it to provide additional information and support the application process. Below is a list of these documents, each described briefly.

- ACORD 133: This form is used to apply for coverage under the Assigned Risk Plan. It provides details about the business and its operations, helping insurers assess the risk.

- ACORD 101: The Additional Remarks Schedule allows applicants to provide further details or explanations that may not fit in the main application. It is useful for clarifying complex situations.

- Loss Run Reports: These reports summarize an applicant's claims history over a specific period, typically the past five years. Insurers use this information to evaluate risk and set premiums.

- Florida Last Will and Testament Form: To ensure your final wishes are honored, complete the essential Florida Last Will and Testament document and secure your legacy effectively.

- State Rating Worksheet: This document helps calculate the estimated annual premium based on the specific state regulations and classifications. It includes details about payroll and employee classifications.

- Employer's Liability Insurance Application: This form is often required to apply for employer's liability coverage, which is typically included in workers' compensation policies but may need separate documentation.

- Safety Program Documentation: Many insurers require proof of a written safety program as part of the application. This documentation outlines the measures taken to ensure employee safety.

- Business Description Statement: This statement provides a detailed description of the business operations, including the nature of the work and any associated risks. It helps insurers understand the business better.

- Prior Carrier Information: This section includes details about previous insurance carriers, policy numbers, and loss history. It helps insurers assess the applicant's claims experience and risk profile.

Each of these documents plays a critical role in the workers' compensation application process. By providing comprehensive information, they help ensure that applicants receive the appropriate coverage tailored to their specific needs.

More PDF Forms

Melaleuca Cancellation Form Pdf - Cancellation of services includes all associated customer benefits.

Completing the NYCERS F552 Retirement Option Election Form accurately is vital for Tier 1 and Tier 2 NYCERS members, as it directly impacts their future pension benefits and those of their beneficiaries. For more detailed information and to access the form directly, you can visit https://nyforms.com/, which provides the necessary guidance and resources needed during this important decision-making process.

What Does a Esa Letter Look Like - The letter should be on professional letterhead to ensure legitimacy.

Frequently Asked Questions

What is the purpose of the ACORD 130 form?

The ACORD 130 form serves as a comprehensive application for workers' compensation insurance. It collects essential information about the applicant's business operations, employee classifications, and previous insurance coverage. This information helps insurance providers assess risk and determine appropriate coverage and premiums.

Who needs to fill out the ACORD 130 form?

Any business seeking workers' compensation insurance must complete the ACORD 130 form. This includes sole proprietors, corporations, partnerships, and limited liability companies (LLCs). If your business employs individuals, regardless of size, this form is crucial for obtaining the necessary coverage.

What information is required on the ACORD 130 form?

The form requests a variety of information, including:

- Agency name and address

- Applicant's name and contact information

- Business type (e.g., corporation, LLC, sole proprietor)

- Years in business and relevant classification codes (SIC and NAICS)

- Details about employees, including their roles and payroll

- Prior insurance coverage and loss history

This information is critical for insurers to evaluate the risk associated with your business.

What is the significance of the classification codes (SIC and NAICS)?

Classification codes, such as SIC (Standard Industrial Classification) and NAICS (North American Industry Classification System), categorize businesses based on their industry and operations. These codes help insurers understand the nature of your business, which influences risk assessment and premium calculations. Accurate classification is essential to ensure that your business is appropriately covered.

How does the ACORD 130 form impact my workers' compensation premiums?

The information provided on the ACORD 130 form directly affects your workers' compensation premiums. Insurers use the details about your business operations, employee classifications, and loss history to calculate the risk level and determine the premium amount. Inaccurate or incomplete information could lead to higher premiums or insufficient coverage.

What should I do if I have a loss history?

If your business has a loss history, it’s important to disclose this information on the ACORD 130 form. Insurers will review past claims to assess risk. Providing detailed explanations about the nature of the losses can help insurers understand your business better and may lead to more favorable terms. Transparency is key in this process.

Can I exclude certain employees from coverage?

Yes, the ACORD 130 form allows for the exclusion of specific employees from coverage. However, this must be done in accordance with state laws and regulations. For example, in Missouri, exclusions must meet specific requirements. It’s important to consult with an insurance professional to ensure compliance and understand the implications of excluding employees.

What happens if I provide false information on the ACORD 130 form?

Providing false information on the ACORD 130 form can have serious consequences. It may lead to denial of coverage, cancellation of your policy, or even legal repercussions for committing fraud. Insurers take misrepresentation seriously, so it’s crucial to ensure that all information is accurate and truthful.

How often should I update my ACORD 130 form?

It’s advisable to update your ACORD 130 form whenever there are significant changes in your business operations, employee count, or insurance needs. Regular updates ensure that your coverage remains adequate and that your premiums reflect your current risk profile. Additionally, when renewing your policy, you may need to submit an updated form.

Where can I obtain an ACORD 130 form?

The ACORD 130 form can be obtained from various sources. Most insurance agents or brokers will provide it to you directly. Additionally, the ACORD Corporation's website offers downloadable versions of the form. Ensure you are using the most current version to avoid any issues during the application process.